A sideways look at economics

Economists, and this author is one, regularly score well below average on surveys of public opinion in relation to their trustworthiness – below both lawyers and pollsters in one recent survey in the UK, for example. This is humbling, and causes us to consider how we can do our jobs better. And it reflects, I think, a view of economists that all we care about is money. As the saying goes, we know the price of everything but the value of nothing. But there’s always someone worse off than yourself: politicians regularly come bottom in the public estimation. I think that’s because politicians – with their hands on the purse-strings of the state – often do not respect the value of money at all. That’s what economists are for.

Here are two topical examples. The first is important and not funny at all – apologies for that. The second is trivial in the grander scheme of things, but makes the same point.

The first is Venezuela.

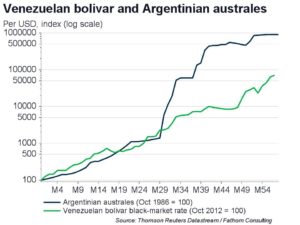

Three years ago, the official US dollar:Venezuelan bolivar exchange rate was around 1:6, and the black-market exchange rate was around 1:60.

The Venezuelan currency is now apparently worth less than the pretend gold used in the game ‘World of Warcraft’ – the bolivar having tanked a further 50% against the dollar on the black market in the last month alone. You now need 12,200 bolivars to buy one dollar on the black market, making one bolivar worth less than one-hundredth of a cent. Having the print of the currency on it actually reduces the value of the paper for low-denomination bills: those bills are literally not worth the paper they’re printed on. This point is emphasised by the fact that Venezuelan police are apparently paid bonuses in the currency of toilet rolls rather than bolivars, the former being more valuable.

It is worth dwelling for a moment on the magnitude of the catastrophe in Venezuela. This is a country that enjoys the largest reserves of crude oil in the world (ahead of Saudi Arabia). With a population of 31 million (compared to 28 million in Saudi Arabia), such enormous oil wealth ought to confer a high standard of living on the average person, even in an authoritarian regime where the wealth flows disproportionately to those at the top – the comparison with Saudi Arabia is apt. And, in 2016, it did – with average income per capita of around $15,000 (at purchasing power parity exchange rates), just over $10,000 at official market exchange rates, and close to $2,000 even at black-market exchange rates. But since then, measured at either official or black-market exchange rates, it has fallen by a factor of at least ten: the typical Venezuelan citizen endures a lower per capita income in dollars than those in the poorest countries on earth.

The collapse in the Venezuelan currency mirrors the abject failure of the (allegedly) corrupt and brutal leftist regime of Nicolas Maduro in that country. He demands a gigantic financial sacrifice from his people to protect what in the grand scheme of things is a vanishingly trivial issue – his personal power and wealth. And the impact is not just on the value of the currency: it is in the real economy too. Official data for CPI inflation are no longer published, but an opposition politician cites inflation running at 176%, while the IMF forecast inflation at over 700% this year. Together that suggests exponentially increasing inflation. And official GDP is contracting at nearly 20% per year – again, something that is likely to get worse. The tragedy is that it is completely unnecessary, and is driven by politics.

Venezuela has a strong claim for being the worst-managed economy of all time. Others have fared worse due to terrible economic choices – Zimbabwe, for example. But countries with natural resource wealth comparable to Venezuela have not seen collapses like this except in times of war.

If you think currency markets are judging Venezuela harshly, the bad news is that the worst might be yet to come. Argentina was judged even more harshly back in the early 1990s. The collapse in the value of the bolivar is small so far compared to the standards set by Argentina back then. If Argentina is a model, then the bolivar could fall in value by a factor of ten from here.

It would be foolish to buy bolivar-denominated assets just yet. However, some investors make poor choices all the time.

This brings us to my second example, the footballer Neymar. Neymar is transferring to PSG from Barcelona for a total outlay of around £450 million on the part of PSG, spread over five years, with the fee component being more than double the previous record. Even in the scheme of hyper-elevated football transfer fees, this one is extraordinary. It is worth dwelling for a moment on what it means. The net present value of that transfer exceeds £350 million, or close to half the value of the club (according to Forbes magazine). For it to be judged worthwhile, PSG would have to see their annual revenues increase by at least £90 million, or around 20%, as a result of the transfer. There is no realistic prospect of that happening.

Why did they buy him, if it’s impossible to make an economic case for the fee? The answer has at least two components. First, PSG are making a statement to the world of football: we are big enough to buy anyone, even from a club like Barcelona who do not want to appear to be a ‘selling’ club. The only way you can buy from a non-selling club is if you pay substantially over the odds: if you pay a lot more than the player is ‘worth’. PSG are announcing that they are in a position to do this: the rest of the footballing world should take note.

Second, the Qatari government, members of which are the owners of PSG, are announcing to the world that they are still around, and still able to wield substantial financial clout, even in the face of the sanctions from other Gulf states. It is a political statement on the world stage.

In those two contexts, the fee – less than half a billion sterling – starts to look relatively small.

The depressing conclusion is that the top ranks of world football have become, well, a political football. Future winners will be those clubs with the strongest political backing. Because it is only politicians with control of the purse-strings of sovereign states who treat huge sums of money with such contempt. The same applies in Venezuela.