A sideways look at economics

All kinds of ideas have been floated on how the government could raise revenue in the UK’s Autumn Budget. From hikes on income tax or a new wealth tax, to spending cuts, income tax/National Insurance ‘two up, two down’, or even changes to the fiscal rules — the list goes on. Less discussed than most has been extending the freeze on personal tax thresholds; but this is perhaps the most effective weapon in a Chancellor’s armoury for increasing the tax take.

As the grumpy ogre Shrek might have said, taxes are like onions, and onions have layers. The UK tax code is said to be the longest and most complicated in the world – with so many different rules, combined with near-constant tinkering to reflect the broader economy and politics — it is extremely hard to tell what is going on or how it is likely to affect you. As the name implies, the impact of a stealth tax is harder for the taxpayer to perceive. This may be why the threshold freeze is often favoured over explicit tax hikes, as governments seek to sustain popularity, while increasing spending capabilities without raising debt. Personal tax allowances and the higher rate threshold have already been frozen since 2021 and are due to stay unchanged till 2028. Meanwhile, the additional rate threshold has been frozen at £125,140 since April 2023 following a reduction from the long-held £150,000 threshold.

Let’s start with maybe the most important question: what does freezing the tax thresholds raise? The Office for Budget Responsibility (OBR) has done some estimates on the effects of various changes to the tax regime. Typically, the most effective income tax hike in generating revenue is thought to be a one-percentage-point increase in the basic rate, so the chart below compares that against the effect of the sustained personal tax threshold freezes.

It’s easy to see why a government would find this kind of measure attractive. It would require almost a six-percentage-point increase in the basic rate to 26% in this month’s Budget to deliver, in 2027/8, the same additional revenue that the current freeze in allowances (implemented in 2021/2) will deliver in 2027/28 if maintained. So how does the revenue-raising method work?

Typically, UK income tax thresholds have been indexed to inflation. In a world where productivity growth is positive, and real wages are rising, even this approach will gradually drag more and more earners into higher tax brackets through a process euphemistically referred to as ‘fiscal drag’. But when income tax thresholds are frozen, as they have been since 2021, the whole process occurs much more rapidly, particularly during periods of double-digit inflation.

Let’s take the example of a basic-rate taxpayer with a gross income of £50,000, and assume that inflation and wage growth are both 3%. After a year their gross pre-tax income will increase to £51,500 but their real pre-tax income will stay the same as before (at £50,000). As a result, £1,230 (the amount over the £50,270 higher rate threshold) will now be taxed at 40%, rather than the prior basic rate of 20%. On top of this, the proportion of their real income covered by the tax-free personal tax allowance will shrink by 3%, so that £377.10 previously tax-free is now taxed at 20%. Fiscal drag will also erode the value of their National Insurance Contribution (NIC) tax-free allowance, another £377.10 taxed at 8%. Freezes in the NICs allowance affect all earners, but lower-paid earners in particular.[1] Above £50,270 the rate of NICs falls from 8% to 2%, so higher earners actually benefit when the higher threshold is frozen. However, the drag from the personal income tax freeze outweighs this.

All else equal, the combined impact of threshold freezes for our taxpayer earning £50,000 whose pay is uprated in line with inflation is that the nominal tax they pay increases by 5.7%, and their real disposable income falls by around 0.7% after one year. Of course, 0.7% doesn’t sound like an awful lot, but it still stands just shy of £270 of real disposable income lost for a £50,000 earner! This could fund two Netflix subscriptions, or the average household’s food shop for a month, or all of those “Okay, just one more” moments.

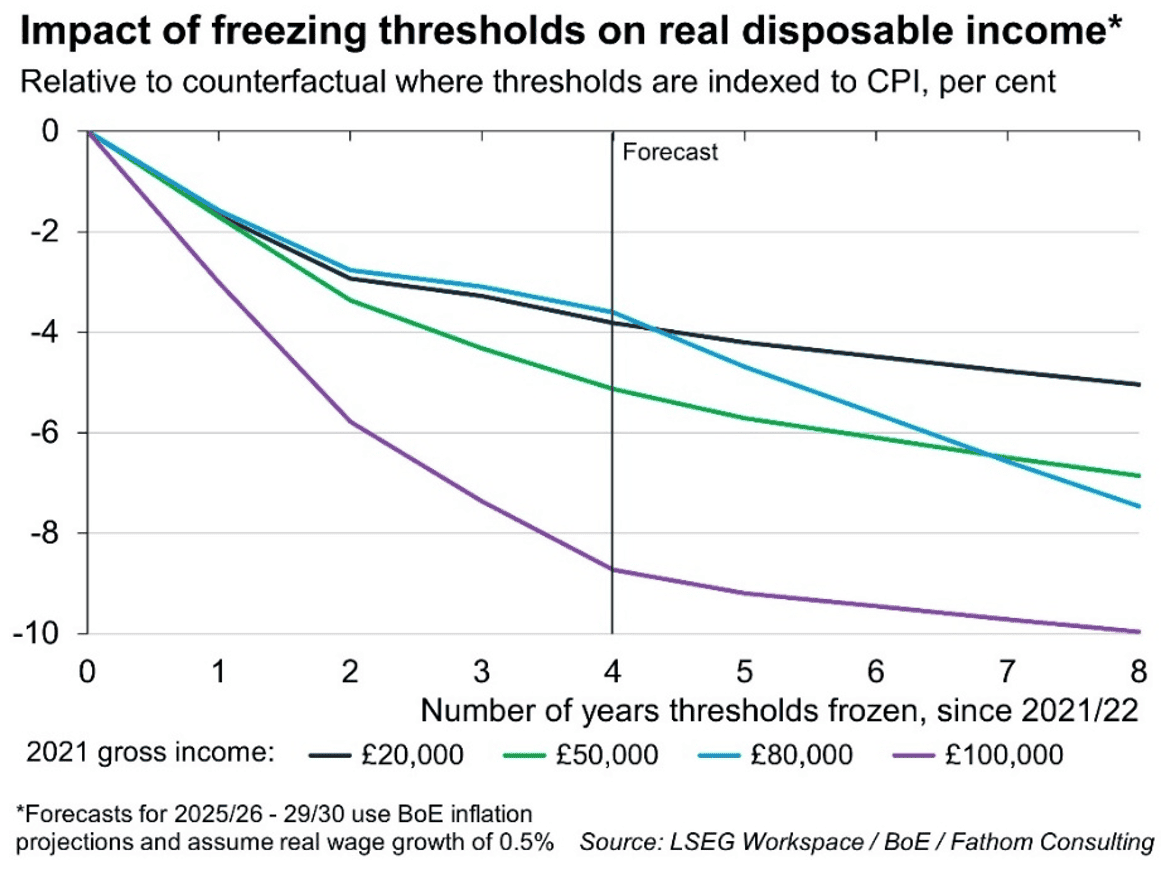

The extent of the impact is largely dependent on wage and inflation dynamics. Let’s take a look at the likely impact that threshold freezes have had and will have on various earners according to their gross income in 2021, relative to a hypothetical counterfactual case where tax thresholds are adjusted in line with inflation.

Everyone is worse off relative to the counterfactual, but it’s clear from the chart that the impacts of tax threshold freezes are not evenly distributed. The most affected earners are those whose initial income sits close to the tax thresholds and so see more of their income pushed into higher tax brackets. Hence, why £50,000 earners may lose proportionally more of their income than those on £80,000 at first, while £20,000 earners feel the dual fiscal drag effect on the tax-free allowances for NIC and personal income more.

Meanwhile, we see our prospective £80,000 and £100,000 gross income earners in 2021 impacted most in the longer term. This is mainly due to the marginal tax rate of 60% on each additional pound earned when taxpayers pass the £100,000 pre-tax income mark.[2].

Much like the boiling frog tale where a frog would jump out if put straight into boiling water but, when slowly boiled it will not jump out, taxpayer income is gradually squeezed further without the taxpayer being fully aware of the increased taxation via stealth taxes. If taxpayers were thrown directly into boiling water, or saw noticeably higher income taxes, they might react more.

I guess the final impact is the same question one poses, and many researchers have investigated, in response to almost any tax increase. Despite this, I still can’t help but be concerned about the impact fiscal drag has on consumer sentiment, standard of living and the relative attractiveness of other countries — prompting the dreaded brain drain — as taxpayers are slowly boiled and still feel the income squeeze. Incomes may still be high but, for most people, it is the relative that matters most not the absolute.

If you’ve made it this far, well done! I hope this blog has peeled back some of the onion layers. Unfortunately there are more. I have only highlighted the personal tax threshold freeze, but there are other forms of stealth tax, from inheritance tax thresholds frozen since 2009 and VAT registration threshold freezes for businesses to the more recent employer NIC hikes, which some would argue is a stealth tax on workers. Let’s hope that come Budget Day the onion does not have us all crying.

[1] The main-rate cut in NICs in 2024/25 has softened the blow, especially for lower earners, but the impact is still net negative relative to their purchasing powers in 2021.

[2] The marginal tax rate of 60% stems from for every £2 earnt over £100,000, taxpayers lose £1 of their personal tax allowance, and see it taxed at the higher rate of 40%, leading to £1.20 paid in tax for every additional £2 earnt (Marginal tax rate ).

More by this author