A sideways look at economics

Donald Trump has announced Kevin Warsh as his nominee to be the next Chair of the Federal Reserve. Mr Warsh is a former Fed official and came close to securing the nomination in President Trump’s first term before ultimately losing to Jerome Powell. I wrote a piece at the time that covered his views, noting that he was a firm critic of unconventional monetary policies, such as quantitative easing (QE), that were implemented in the aftermath of the Global Financial Crisis.

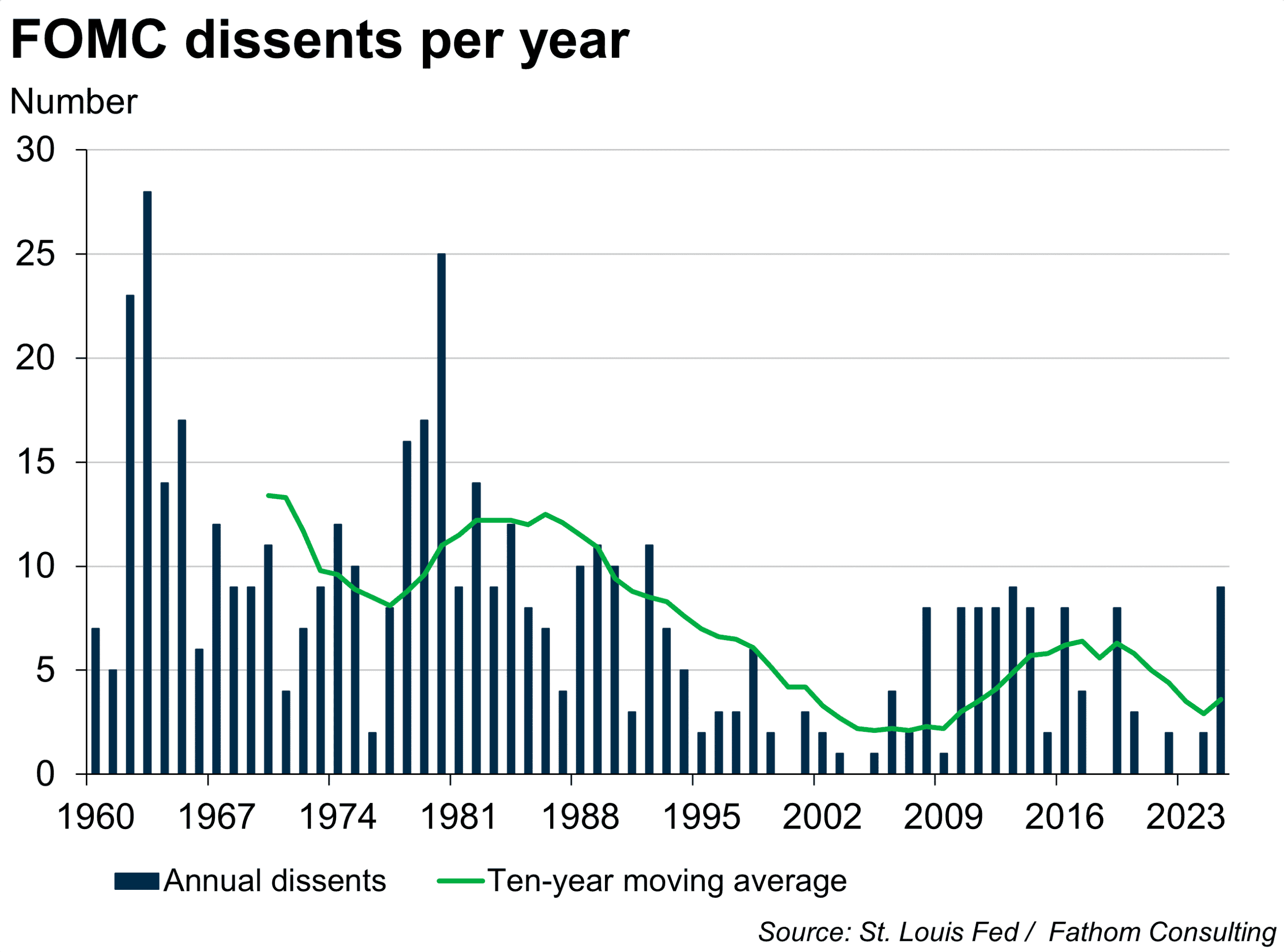

One conclusion from the piece was that the Fed could stand to benefit from a chair who was willing to challenge the consensus and orthodox thinking. What has happened since then? Groupthink, as measured by the lack of dissents at Federal Open Market Committee meetings, continued to worsen, with zero dissents in 2021 as price pressures spiked and interest rates remained at zero while QE continued. Just as the Fed was losing control of inflation, officials were more aligned than ever that policy was appropriately calibrated. We all know how that turned out.

Mr Warsh’s views seem to have evolved. Previously, he was a noted hawk, but now he seems to be in favour of easier monetary policy. Some of his arguments relate to the disinflationary impact of AI. Whether that evolution reflects genuine intellectual development or political expediency, only he would know. But with technology and globalisation seemingly in a period of rupture, there should be room for substantial but reasonable disagreement on the committee. Governor dissents are particularly rare, so this suggests genuine intellectual disagreement may be returning.

The original blog concluded with a thought:

If Mr Warsh is nominated, and sticks with his decidedly hawkish view once in Washington, investors will have to seriously consider whether they will soon see a Fed chief outvoted. The alternative? Too horrible to contemplate: a Fed Chair who continues to carry the FOMC, but who does not get pushed around by markets.

Now that his nomination has been confirmed, a mere eight years after his name was last touted for the role, the possibility of a Chair Warsh being outvoted still seems high. But there is another risk worth contemplating: that the anticipated ‘easy money’ Kevin Warsh turns out to be more like his hawkish former self.

We have begun our forecast process for Fathom’s Global Outlook, Spring 2026, and will update clients on the outlook for monetary policy and its impact on the economy and financial markets in the coming weeks.

More by this author