China’s Future Industries plan, introduced in 2024 and reiterated in this year’s five-year plan, is the next chapter in Beijing’s long-running push to upgrade its industrial base. It targets six broad sectors — energy, materials, health, IT, space and manufacturing — several of which overlap directly with the priorities set out a decade ago under Made in China 2025. The underlying objective hasn’t shifted either: cut reliance on foreign inputs while building new domestic “productive forces.”

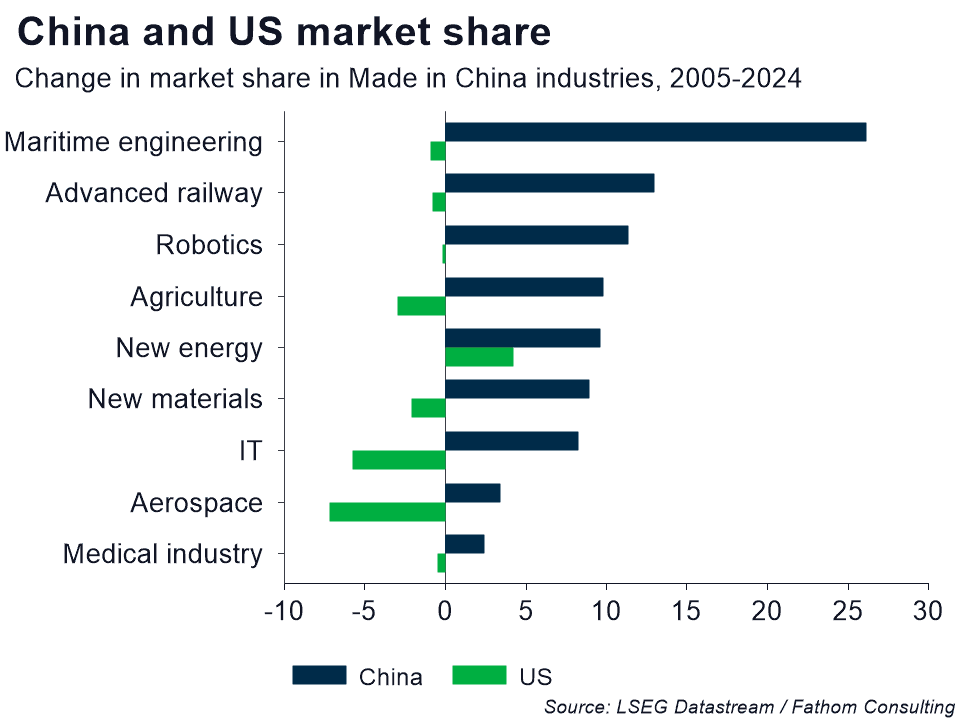

We have a real benchmark for judging how that earlier plan fared. Using our proprietary RiCArdo trade database, originally built to track China’s progress across the nine Made in China 2025 industries, we find that China has increased its global market share in every one of them over the past two decades, often at the US’s expense, and has moved up the value chain in the process. Yet gains in market share haven’t translated into trade surpluses: China still runs a sizeable deficit across these sectors, with IT the persistent sore point — the country remains heavily reliant on imported chips, particularly from Taiwan.

Where Made in China 2025 set out relatively clear, measurable goals, China’s Future Industries plan is more vague. That combination of indistinct ambition and immature technology makes progress inherently hard to track, perhaps deliberately so. We unpack what this ambiguity might be hiding.

Read on for our full assessment, including what a decade of trade data tells us about who’s actually winning the race so far.