A sideways look at economics

Halloween is a tradition originating from the Celtic festival of Samhain. 2000 years ago, this festival marked the end of the summer and the beginning of the winter, when evil spirits came to destroy harvests. It is characterised by horror and darkness, which those who have lived through the terror of 2020 will be quite accustomed to. Although Halloween may look a little different this year, one consistency is that many zombies will be present, but due to social-distancing rules, maybe not the ones we have grown to expect…

In this Friday blog I will be turning my attention away from the array of zombie costumes that would typically grace the streets during Halloween, and towards the corporate undead. The term ‘zombie firm’ was first attributed to Japanese companies hanging onto survival through loose lending during the ‘lost decade’ in 1990. Since then, this phenomenon has not solely plagued Japan. It has spread across the world, including the US, resulting in the rise of the American zombies. In this blog, we will be hopping over to the other side of the world and travelling to China, to assess the scale of zombification in the Asian giant.

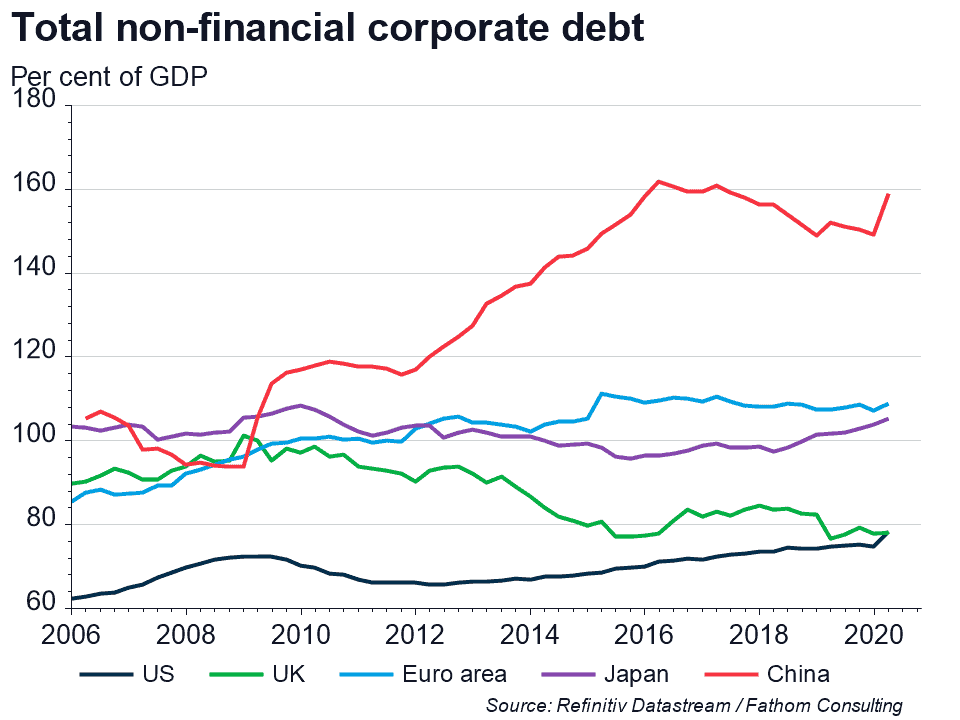

Over the past decade, China’s debt has been increasing at a rapid pace. Relative to its peers, a large proportion of this debt is from corporates. This drastically increased after the 2008 Global Financial Crisis, when Chinese policymakers navigated the downturn by encouraging banks to lend and corporates to gorge on cheap credit.

A proportion of this credit was being allocated to firms that wouldn’t have otherwise been financially viable, resulting in the emergence of zombies. Due to the nature of Chinese statistics, getting accurate, timely data on the number of zombies is more difficult than finding an example of common sense in a horror movie. However, we do have data on the number of loss-making enterprises in each region, giving a proxy measure of zombie firms.[1] These data present a bleak picture for China — the proportion of industrial enterprises that are loss-making has been rising. In December 2019 this hit a staggering 35% of industrial enterprises in the worst-hit region. This trend has only been exacerbated by COVID-19, increasing to over 40%. Evidence suggests that this persistently high proportion of loss-making enterprises is most likely due to local government support. Instead of letting these enterprises fail, local governments are artificially helping them to survive, in an effort to maintain social stability and protect employment.

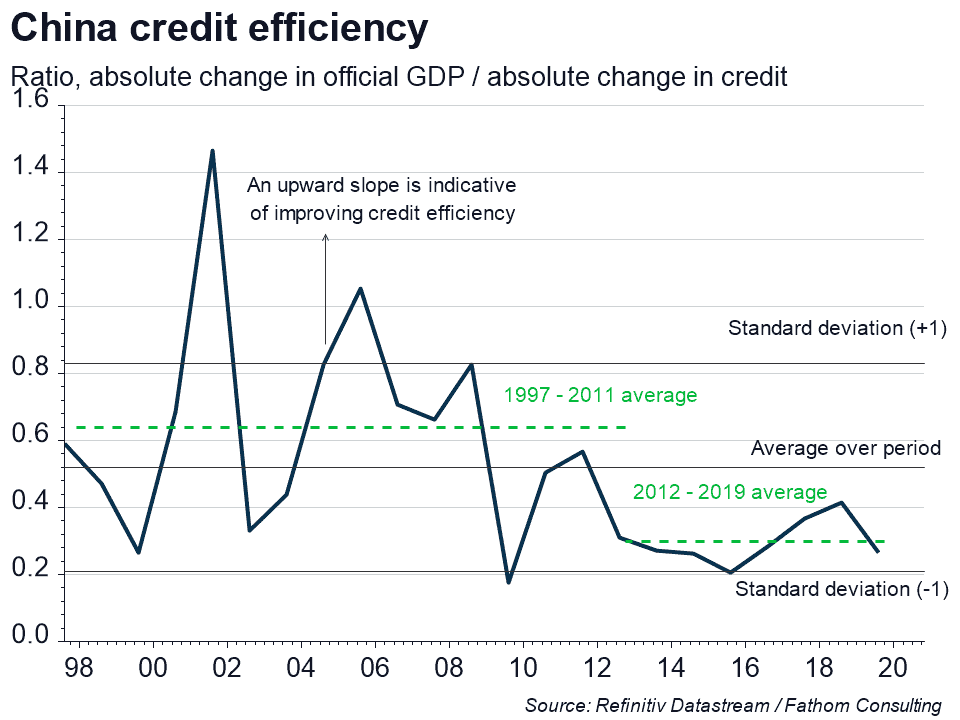

Despite the social benefits of maintaining employment, artificially allowing these firms to survive comes at a cost. The BIS[2] has found that a high zombie share weighs on aggregate productivity growth, as these loss-making firms lead to overcapacity and chronic resource misallocation. This finding, alongside our estimate of Chinese credit efficiency, which has been deteriorating over time, suggests that preventing market forces from operating and artificially allowing firms to survive is an unsustainable economic model. Instead of the typical movie portrayal where a zombie’s mission is to feed on humans, in an economic sense these zombies feed on potential efficiency gains.

Chinese policymakers have recognised this threat to financial stability, and launched a deleveraging campaign in 2016. This campaign included an identification of 345 zombie companies that needed to be killed. (Fun fact, according to the marvels of Google, the most efficient way to dispatch a zombie is with a chainsaw.) Early evidence suggested progress, with insolvency cases (used as an alternative measure to chainsaw sales) rising by 54% in 2016, relative to the year before. This was accompanied by a pause in the ramp-up of non-financial credit as a share of GDP. However, even before the COVID-19 pandemic, we were arguing that China had put deleveraging on the back burner: rebalancing away from credit-induced growth drivers and towards domestic consumption is hard.

With the outbreak of the pandemic, it is understandable and appropriate that deleveraging is now an even remoter prospect. The credit taps are firmly back on, and central and local governments are leaning on old, inefficient methods of growth to stimulate the economy. Regular readers will be aware that this includes investing in industries that are already suffering from gross overcapacity, such as housing construction.

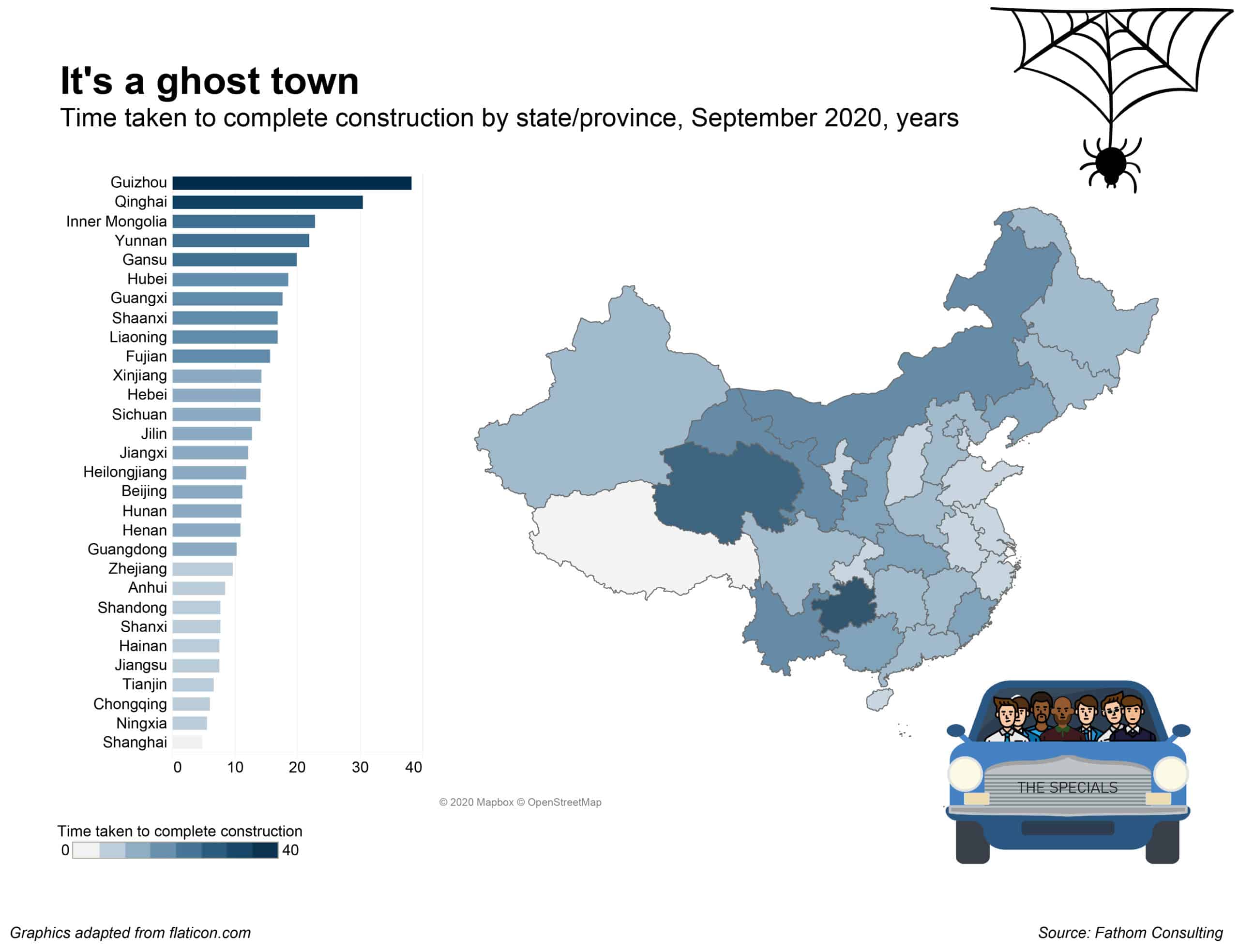

The UK band The Specials once sang of London: “This town, ah, is coming like a ghost town”. Perhaps they could now reissue that hit with reference to many Chinese towns. The average time to finish residential construction projects across China has now reached a staggering ten years. As afficionados of the zombie genre will know, half-empty residential areas are prime breeding grounds for zombies. Despite further residential investment being an inefficient allocation of resources (albeit quite a good song — even if it was released in the 80s), during difficult times it keeps many people tied up in employment. This is in comparison to investing and providing jobs in high-tech infrastructure as an example, which would require timely retraining.

It might be that China’s response to COVID-19 will not exacerbate the zombie challenge in the long term. This would be conditional on support and investment being withdrawn once firms are through the difficult economic cycle, allowing the process of creative destruction to remove the dead wood from the economy. However, with the credit taps already flowing before the crisis, we don’t expect China to tighten the screws any time soon. Progress towards rebalancing away from an overreliance on credit is likely to be muted, with Chinese authorities unlikely to call in the ghostbusters. Brace yourself for the zombie apocalypse.

[1] Under the strict definition, firms are only considered zombies when they have an interest coverage ratio of less than one for three consecutive years.

[2] The BIS estimate the impact of the zombie share on aggregate productivity growth using an instrumental variable regression in which: Total factor productivity growthct+1 = β1zombie sharect + β2output gapct + β3total factor productivity growthct + αc + ϒt + εct (https://www.bis.org/publ/qtrpdf/r_qt1809g.pdf).