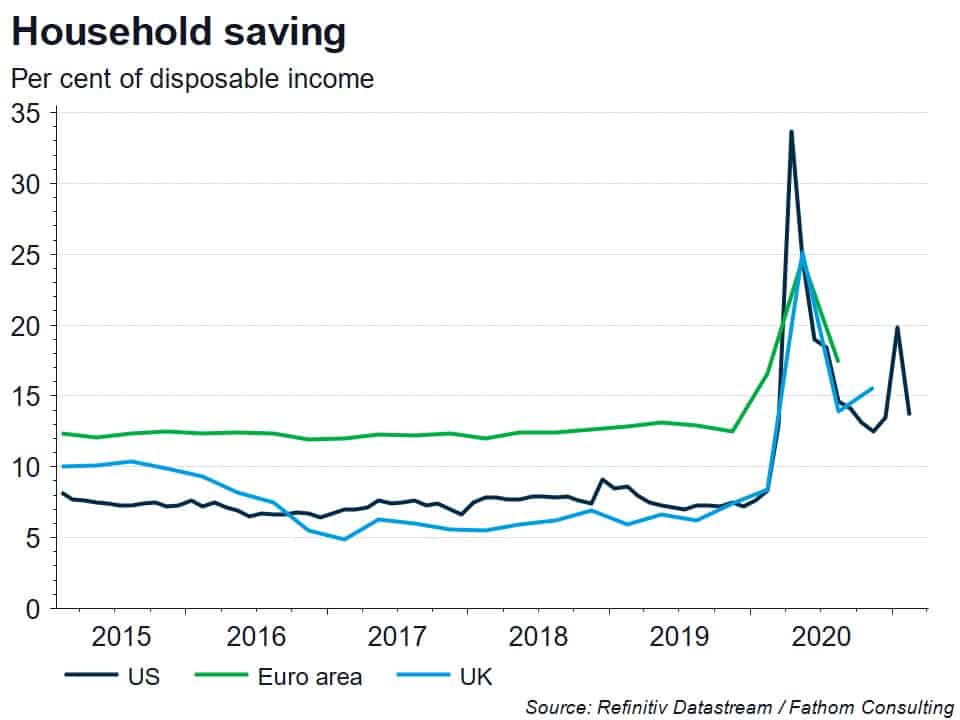

Households in the major economies have built up substantial excess savings pots during the past twelve months, supported by a variety of government programmes set up to limit the economic harm caused by the pandemic. By the end of March, these probably amounted to some 6%-8% of annual GDP in the US and the UK, and some 3%-4% of annual GDP in the euro area. What will happen to these savings as economies reopen? In answering this question, policymakers have taken what seems to us to be an overly cautious approach. Using textbook models of consumer behaviour, the Bank of England’s Monetary Policy Committee assumes that just 5% of these excess savings pots are spent over the next three years. But as we have argued in a recent blog post, these textbook models were not designed to cope with behaviour during a pandemic. The dramatic increase in household savings through last year and into this was a rational, endogenous response to an extremely difficult set of circumstances. Rather than spend the money on things that they were allowed to enjoy, like more goods consumption, households chose to save – presumably in order to spend at least some of the money on the temporarily prohibited activities once that prohibition was lifted. In our own central scenario, to which we attach a 50% weight, we assume that households in the major economies spend around 10% of their pandemic savings in the next two years, with most of it spent this year. In our upside risk scenario, to which we attach a 30% weight, this proportion rises to 50%. It goes without saying that had the Bank of England assumed anything other than a very gradual unwinding of these excess savings pots, their latest inflation fan chart might have looked very different, with a significant chance of inflation lying above target for most of the forecast horizon.

This chart is taken from Fathom’s Recovery Watch newsletter. Click here to subscribe to Recovery Watch.