Headlines

- The rosier near-term outlook that we unveiled in our Global Outlook, Summer 2023 continues to unfold, but we are not out of the woods yet

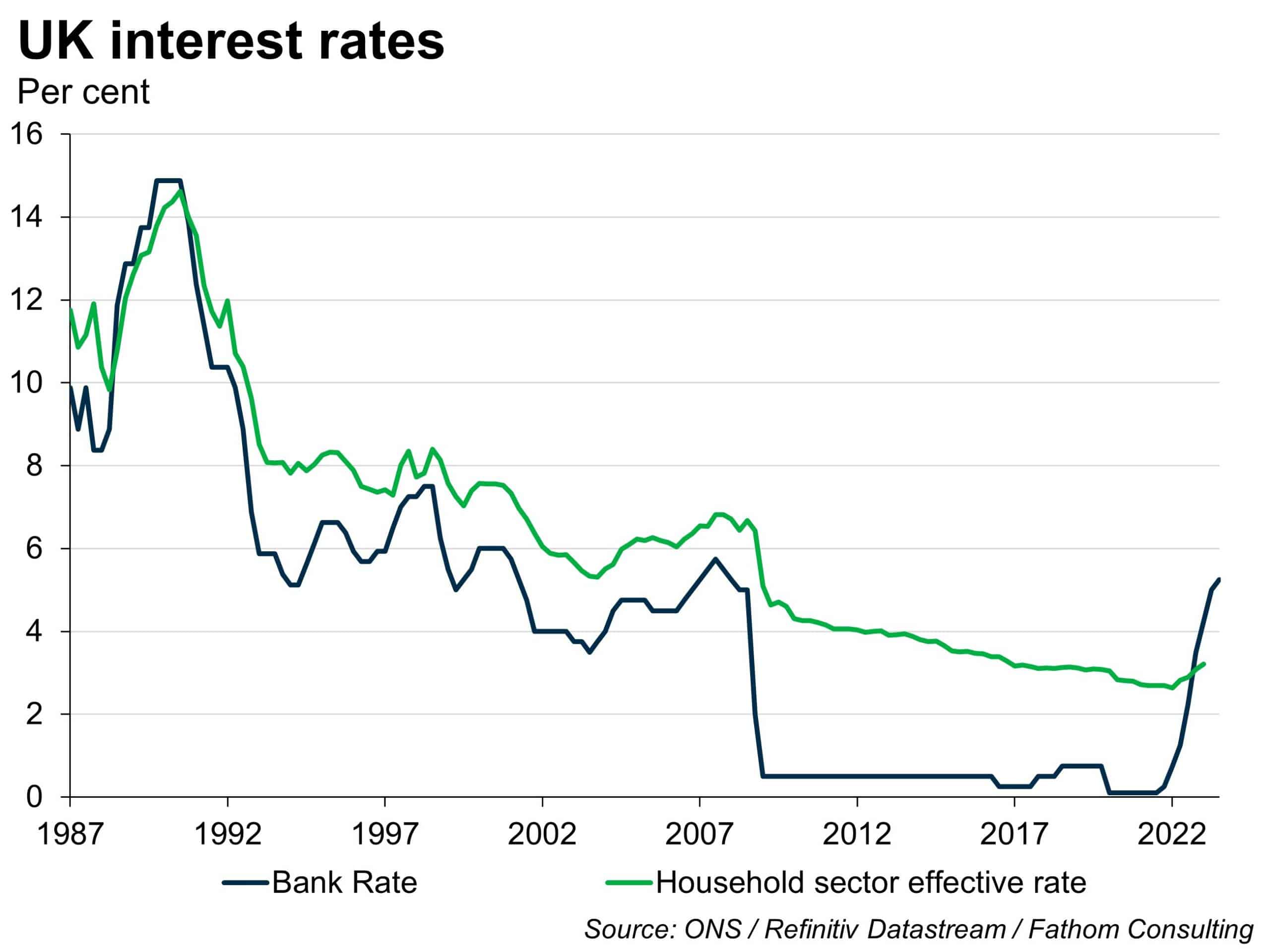

- We argue that longer debt maturities complicate and lengthen the transmission from tighter monetary policy to weaker aggregate demand, but they do not stop it

- Recession can still be avoided, but only if firms set prices and workers submit wage claims on the basis that inflation is going to be 2% — credibility is more or less everything

- This is a more likely prospect in the US than in Europe

[Please click below to read the full note.]