Headlines

- Recent data suggest the risk of recession is lower than previously thought, but it remains our central case for the UK and the EU

- The UK posted zero growth in Q4, likely to be revised down

- The US hangs in the balance still, with equity markets and sentiment sending negative signals, but payrolls and activity data pointing the other way

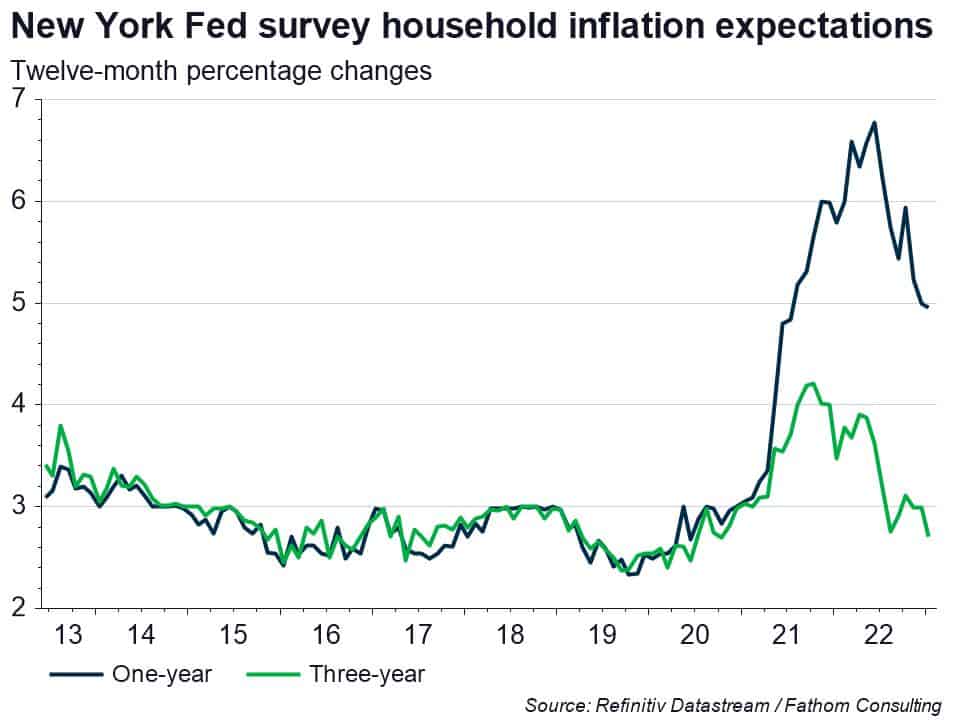

- Medium-term expectations of US inflation show no signs of stickiness but, compared to other countries, US inflation has been flattered by the currency

- Your regular reminder: there is no official definition of what constitutes a recession

- Short-term forecast for the US suggests a couple of negative quarters are still likely, and annual growth will dip to zero before recovering

- Standing back from the noise and some of the more aerated commentary, this sort of pattern is to be expected after the COVID convulsion: a pause for breath, so to speak

[Please click below to read the full note.]