A sideways look at economics

In Salman Rushdie’s book Haroun and the Sea of Stories, we are introduced to the concept of the P2C2E. How does a magic carpet actually fly? It’s a P2C2E. When you say there’s a genie trapped in that lamp, how does that actually, mechanically, happen? Another P2C2E.[1] It’s a bit like the ‘flux capacitor’ in the Back to the Future series: something extremely important and impossibly difficult to explain. There are a couple of real-world examples of this floating around at the moment — quantitative tightening (QT) is one. What is it? Well, it’s hard to explain. But let me have a go anyway.

So, it’s the opposite of quantitative easing (QE). Does that help? Not really, right?

You have probably heard an explanation of QE that goes like this — the central bank (let’s go with the Bank of England) prints money and uses it to buy bonds. It’s a nice, clear picture. We imagine someone in the Bank issuing an order, relayed to someone at the mint, who cranks up the printing presses and some crisp new tenners are stacked in large cases, and transported to… well, where, precisely? In the imagination, some physical exchange, where various dodgy characters turn up with boxes full of government bonds. A price is agreed, somehow, and the exchange takes place.

Sadly, this is not correct.

First, there is no ‘printing’ involved. The supply of notes and coin, physical cash money, is a small proportion of the overall supply of money, most of which is in the form of electronically recorded deposits without any physical corollary. In the case of QE, the Bank of England does increase the supply of money: its quantity (hence the term ‘quantitative easing’)[2]). Not physical money, but electronic money. So that’s easy, right? We must let go of our nice image of a physical exchange, boxes of cash and boxes of bonds, Del Boy and some geezer from the Bank, downstairs at the Winchester over a mild and bitter. But it doesn’t sound too complicated. It’s an electronic exchange. Now we imagine Josephine Bloggs, who has an account somewhere that has some government bonds in it, being approached with what? A phone call, say, from the Bank of England, saying would you like to sell those bonds to us? In exchange, we’ll credit your current account with the agreed sum, and you will transfer the bonds to us.

That’s not what happens either.

The purchase is made only from the banks. The Bank of England buys bonds from the banks. OK, that sounds a lot more boring but still not super complicated, until you dwell on it for a moment. Let’s say the Bank of Erik (not real, not yet) holds a set of government bonds that, if they were sold on the open market, would be worth £1 million. The Bank of England comes along and buys them and, in exchange, it credits… wait, what does it credit? Some kind of account. But what kind? It can’t credit the account that the Bank of Erik holds with another private bank. That would imply a liability for the other bank, whoever that was. In fact, it credits the account that the Bank of Erik holds at the Bank of England: all private banks have such an account. Right, so now I’ve got it: Bank of Erik sells its bonds to the Bank of England in exchange for electronic cash in the Bank of Erik’s account at the Bank of England. So now Bank of Erik can rush out and spend that cash on other stuff, right?

Wrong. Nearly right, but not quite. Bank of Erik cannot decrease its electronic cash holdings at the Bank of England unless some other bank, or set of banks, increase their holdings by an exactly equivalent amount. Otherwise, the Bank of England’s assets (in the form of government bonds) would exceed its liabilities (in the form of cash deposits by the banking sector). In effect, Bank of Erik could lend some of its cash on deposit at the Bank of England to other banks if it chose to, so long as they held them on deposit at the Bank of England too. There are circumstances in which Bank of Erik might want to do that, but it’s not like the cash that sits in your account at your bank, that you can do more or less anything with. It’s not that liquid. Thinking of the banking system as a whole, it’s not liquid at all. The banking system cannot go and spend that cash, so to speak, on anything.

So now I think I’ve got it: there’s an exchange, bonds for cash (albeit illiquid cash) on account at the Bank of England. But the net effect is there’s more cash (liquid or otherwise) in the whole system, banks and everything included.

Now, what was the purpose of QE? To be an additional lever of monetary policy over and above control of the policy rate, to keep bond yields low at all maturities and to boost the value of other assets as a result. Did it work? Possibly.

One effect was to remove government bonds from the system and replace them with cash on deposit at the central bank, which is not (in aggregate) liquid. Did that make the private banking system as a whole more liquid or less? The answer is not clear: among banks, government bonds are almost as liquid as cash — especially in circumstances where the short interest rate and yields at all maturities are at or close to zero, which was the prevailing environment when QE was implemented. And the cash that’s replaced them is not as liquid as other forms of cash. In principle, holding more of that kind of cash allows the banks to lend more, since those cash holdings are part of their capital, against which their lending books are measured when judging their capital adequacy. More capital means you can acquire more assets: you can lend more. But there are two problems with this theory, in the UK anyway. First, while government bond holdings are not counted as part of a bank’s capital (they are assets, not capital), they are zero-weighted assets when capital adequacy is calculated, implying that removing them from the asset book has no effect on the risk-weighted size of that book: yes, capital has increased thanks to QE, but capital adequacy ratios have not increased as much as if other assets had been bought, such as corporate debt. And second, the purchase of those bonds from the banks by the Bank of England was happening at a time when the banks were being required, by new regulations, to reduce the risk in their asset books compared to their capital, which meant lending less for each £1 of capital. Bottom line: the net impact on bank lending was ambiguous.

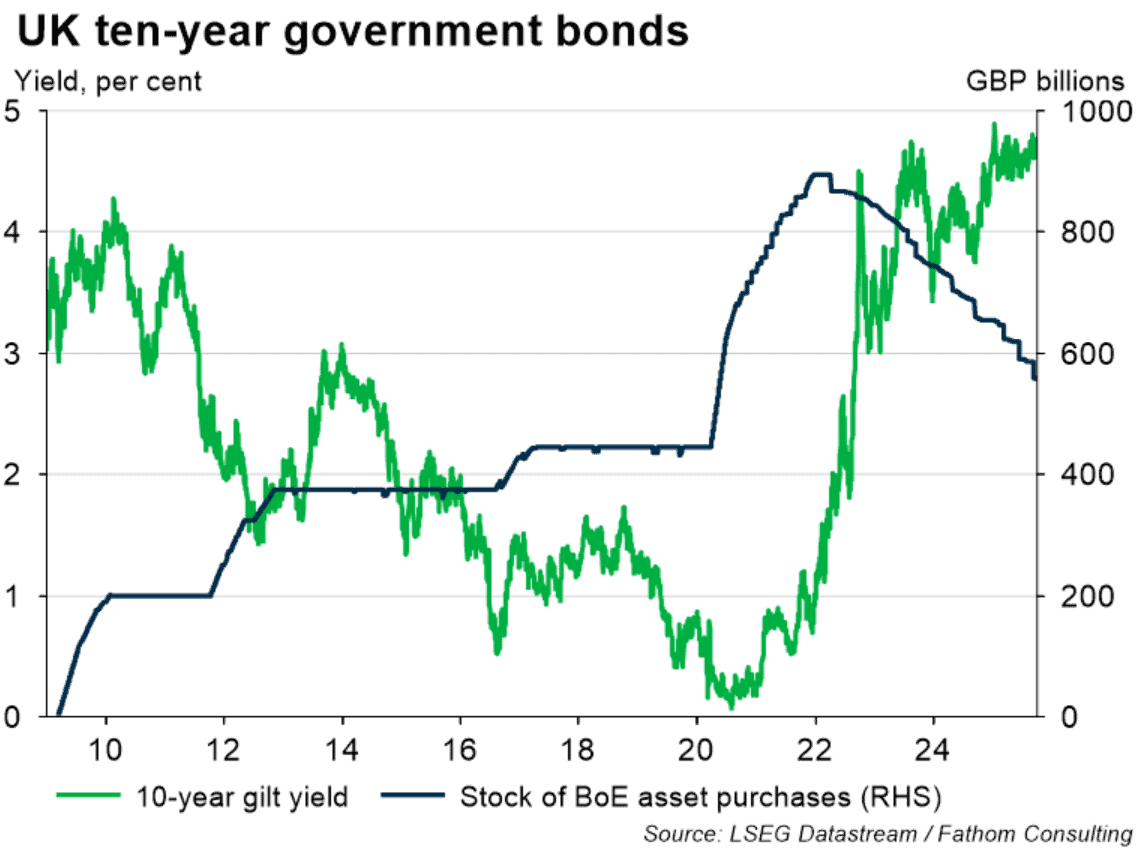

OK — but surely the demand for government bonds from the central bank must have changed the prevailing price of those bonds, pushing the price up and keeping the yields down? Possibly. The awkward thing about QE as it was implemented in the UK is that the increased demand for government debt from the central bank went in equal steps with increased supply of government debt, as a result of a big increase in the government’s borrowing requirement. Pretty much every pound of QE was accompanied by an extra pound of government debt. So, the net impact on the price of government debt is, well, ambiguous again, in the UK at least. By the time the first round of QE was introduced by the Bank of England, two-year gilt yields had already collapsed (the UK was in a deep recession at the time), and it is not clear that QE made much difference there, though the ten-year yield took longer to track downwards — perhaps as a result of QE, but perhaps as a result of persistently low short rates (recall that the long rate is the cumulated expected short rate plus or minus risk). The line from the Bank of England’s research in this area is: yes but, relative to the counterfactual, bond prices were higher than they would otherwise have been, thanks to QE. This is a hard assertion to disprove — virtually unfalsifiable, in fact. But it is probably correct.

Higher bond prices would mean lower bond yields than would otherwise have been the case.[3] Anyone (individual or institution) who has an asset portfolio that includes UK government bonds would, after QE, have seen an increase in the share of that portfolio allocated to those bonds than would otherwise have been the case. This is where the issue gets knotty, or even knottier. The hope of QE was that, via something called portfolio rebalancing effects, the price of other assets would be bid higher. If I desired that 10% of my portfolio were accounted for by UK government bonds, and QE, by increasing the value of those bonds, had the effect of making that 15% (say), then I would rebalance my portfolio by selling a third of those bonds and using the money to buy other assets like equities. Bond prices would fall and equity prices would rise as a result.

It’s extremely hard to find those effects when the impact on bond prices is only there relative to the counterfactual. A close observer would see no change in the typical portfolio structure after the introduction of QE, because of the corresponding increase in the issuance of debt, which had the effect of holding bond prices down. An equal and offsetting effect to that of QE. Ah but it would have changed in the counterfactual, and it didn’t change in fact! So other asset prices are higher than they would have been otherwise! Maybe. But you start to see why the Bank of England (and others) have a communications problem around QE.

Now: QT is just the opposite of that, with some extra wrinkles of its own. Its introduction in the UK coincided with the Truss government’s announcement of unfunded tax cuts, bypassing the role of the OBR; and also with a spate of margin calls on pension funds with leveraged positions on government bonds. What followed was a demonstration that even mature, advanced economies with independent monetary policy can suffer a fiscal crisis if they try hard enough. The introduction of QT certainly coincided with an increase in bond yields, some of which was probably causal, which is what we would expect given there was no compensating tightening of fiscal policy (but instead an unfunded loosening). Ready for the full account? I thought not. Let’s just call it a P2C2E.

P.S. If you’ve read through all of that, you might be interested in this: https://www.youtube.com/watch?v=mVD8XaRfs4c which is a nice explainer of QE and QT by Ed Conway from Sky News. I gather that engagement with this piece was extremely high, which I personally find encouraging: a nine-minute detailed look at a highly arcane bit of central bank lore, and people want to engage, to find out how it works.

This is perhaps part of a wider pattern— some highly detailed and lengthy podcasts are also attracting large audiences, for example this series: https://www.youtube.com/channel/UCdWIQh9DGG6uhJk8eyIFl1w, which I have spent many hours listening to with great interest. Not everything online is soundbites and six-second videos of someone doing something utterly pointless; long-form, difficult material is finding its voice too.

P.P.S. If you’re still interested in this topic, you might want to seek professional help. Otherwise, there’s a recent working paper from the Bank of England on the impacts of QE and QT that you can find here: https://www.bankofengland.co.uk/working-paper/2024/quantitative-easing-and-quantitative-tightening-the-money-channel, in which the authors suggest that the use of reserves management via QE and QT can play an important countercyclical role in addition to conventional monetary policy. Get ready for the formal addition of these levers to the toolkit available to policymakers in steady state.

More by this author

Why I don’t live on Easy Street

Intelligence is a property of systems

[1] The acronym stands for a Process Too Complicated To Explain.

[2] There are two ways to ease the stance of monetary policy. The first is to reduce the price of money, which is the prevailing interest rate, and watch the quantity of money in circulation adjust (usually upwards) as a result. The second is to increase the quantity of money in circulation ‘directly’ and watch the price — the prevailing interest rate or, in this case, the whole of the yield curve — adjust (usually downwards) as a result.

[3] If I were to issue an Erik Bond, a piece of paper saying: “I promise to pay the bearer of this bond £100 on 3 October 2035,” how much would you pay me for that piece of paper? Let’s say you are rather sceptical about my ability or willingness to honour that promise when the time comes. You might agree to pay me £30 for that piece of paper. That would imply you want to be compensated by a net £70 on top of the principal in 2035 (at 2035 prices) to induce you to buy that piece of paper from me. The yield you will earn on that asset (if I agree to the sale) will be (100/30 – 1) after ten years. Annualised, it will be (100/30)^(1/10)-1, which is 12.7% per year. It follows that if you agreed to pay me more, say £50, the implied yield would be lower at (100/50)^(1/10)-1, which is 7.2% per year. The price that you pay is inversely related to the yield. If you’re lucky, you could sell that piece of paper in the secondary market, and get someone to pay you more than you paid me – the market price would be higher and the yield they would achieve, lower.