A sideways look at economics

Many years ago, when I still worked at the Bank of England, I was chatting to a former Bank employee at an evening function in the Court Room (a grand, chandeliered, Turkish-carpeted ballroom). She had recently left the Bank to join a major global management consultancy, so I asked her what her role was. She said she was analysing supply chains. “Gosh, that sounds interesting,” I said, in what was intended to be a dry, ironic tone. She said that it was, it really was; and that she felt passionate about supply chains. I was loudly sceptical. “Nobody in their right mind is passionate about supply chains. Either you’re fooling yourself or you need to seek professional help,” I maintained. How times have changed.

Supply chains are now all the rage. They are probably the number one source of questions we receive from our clients at present: urgent, passionate questions, from clients in government, finance and industry. A couple of years ago, we had a booth at the Special Competitive Studies Project’s AI show in Washington DC, at which we showcased one of our tools, which addressed how supply chains interact with geopolitical alignment.

Georgia and Leara at our booth at the SCSP expo in 2024

We had prepared a banner, emblazoned with the question: “Which of your supply chains is at risk?” We intended to invite passers-by to think, engage their curiosity and get involved in a discussion of the issue. Mostly that’s how it was received. But I remember one guy, a thoughtful-looking chap with a long beard, who stood silent in front of the banner for a couple of minutes, considering it. Eventually, he looked at me and said:

“Cobalt.”

Then he walked away.

At the time, I thought it was a rather unhelpful comment. But I should have paid more attention.

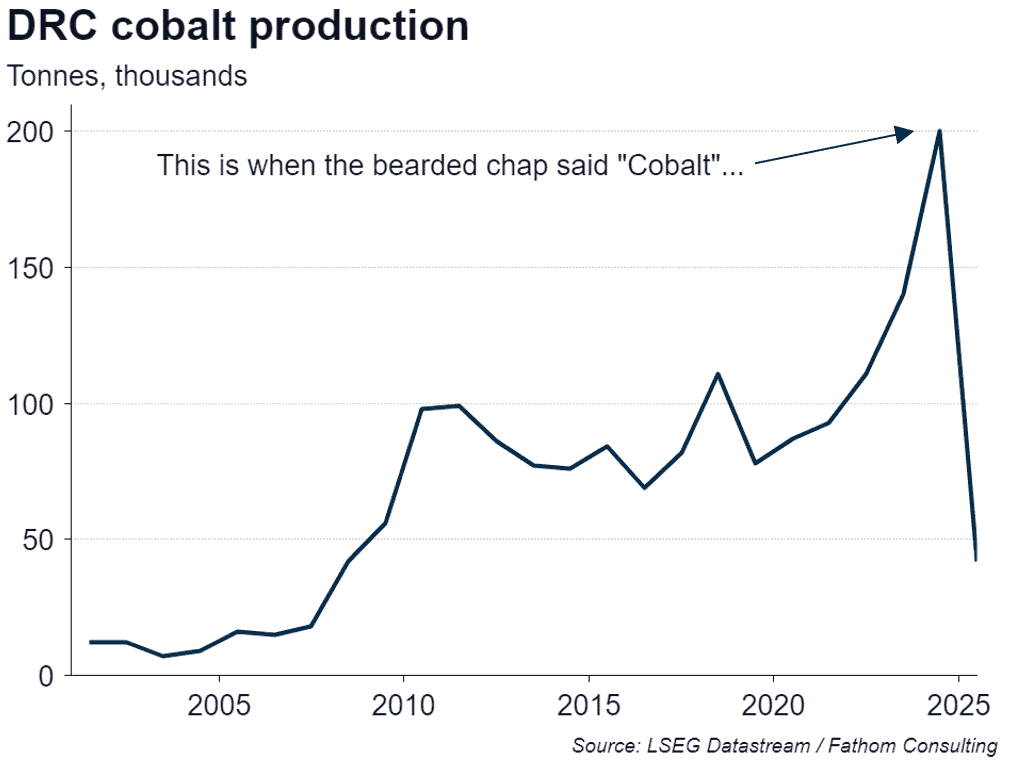

The Democratic Republic of the Congo (DRC) is the source of at least two-thirds of all the world’s cobalt, which is vital for the production of batteries, especially for electric vehicles. The chart below shows the DRC’s cobalt production, which peaked at almost the exact moment the bearded chap identified cobalt as his main supply-chain risk. The collapse in production since then, by 80% from peak to trough, has resulted from new export quotas, introduced by the DRC in 2025 in response to concerns that the price of cobalt was ‘too low’. An 80% reduction in DRC production of cobalt implies a 55% reduction in global production, at least as the direct, first-round effect.

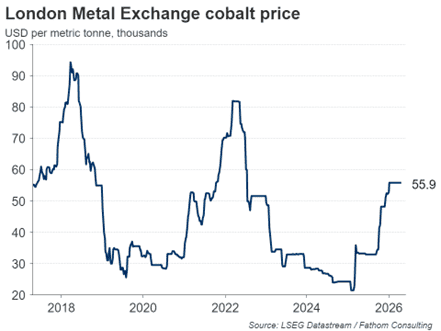

Since the quotas were introduced, the price of cobalt has more than doubled. A 55% reduction in global supply and a 130% increase in price suggests that, as with other commodities, demand for cobalt is relatively inelastic in response to price changes, with a price elasticity of demand of just -0.35.

For DRC, this implies an exploitable market power in this commodity. Despite cutting production by 55%, the value of DRC’s production of cobalt increased by 75%.

Apparently, the plan in 2026 is for DRC production to partly recover, perhaps doubling compared to its 2025 level, which would still leave it some 40% below where it was in 2024. This is a sensible strategy by the DRC: drastically restricting production for a long period of time would cause other countries, such as Indonesia, to increase their production capacity, perhaps permanently, and would also cause the main consumers of cobalt to seek alternative commodities or alternative technologies. Eventually, that would cause the DRC’s market power to diminish. It is a fine line between maximising revenues in the short term and maintaining market power in the long term; one that the DRC appears to be navigating well for now.

This is a general principle for all those who enjoy leverage over others. If you use your leverage, especially if you use it drastically and persistently, then the targets of that leverage will tend to make other arrangements; so it won’t work so well, or at all, in future. Use it carefully, sparingly, like salt. I had a childhood friend whose pocket money had been stopped so regularly by his parents that we calculated he would receive no pocket money until aged 56. Threats to stop his pocket money again had understandably long since ceased having any impact on his behaviour, although in his case it’s not clear they ever did.

The principal consumers of cobalt are the producers of batteries, especially for electric vehicles. And first among these is China. It’s not an accident, then, that China has acquired an interest in cobalt production in DRC. It has done this through inflows of foreign direct investment, both M&A (acquiring an equity stake in existing companies) and Greenfield (building new facilities), over many years. A recent example of this, taken from Fathom’s Capital Flows Tracker, is the investment by MMG (owned by state-controlled China Minmetals Corporation) in the Kinsevere mine. The company announced a USD500 million investment in March 2022 to increase copper production and start producing cobalt at the site. As a result of these inflows, China now owns somewhere in the region of 60% to 90% of DRC cobalt production and refining capacity. The restrictions on production in DRC can possibly be traced back to the influence of China. The bearded chap was right.

This would follow a pattern where China first acquires and then asserts its control over supply chains of critical minerals, globally, in the service of its geopolitical objectives. Fathom has spent many years building a suite of tools that monitor these patterns: patterns of investment, of supply chain control and vulnerability, and of geopolitical implications. I’m not going to expand on all of those here, but suffice to say: are we passionate? No. Obsessed would be closer to the mark.

To my interlocutor at the Bank of England function (you know who you are): I take it all back. You were right. Or perhaps I need to seek professional help.

We have a booth at the forthcoming SCSP show too. Anyone in the DC area between May 6-9, come along. On May 6, we are hosting an interactive session entitled ‘How will AI be shaped by geopolitics, and vice versa’ before the expo proper opens the following day. In this session, participants will navigate through the choices and trade-offs that China and the US face in a bifurcated economy increasingly driven by AI. You can find the agenda for the whole expo here. Entry is free.

Further reading

China’s chokehold on key minerals: what the data say