A sideways look at economics

‘One person’s trash is another person’s treasure: the proverb could not be more true than in today’s context, when global consumption, and consequently waste, are reaching new highs. For example, reflect on all the old electronic products you have disposed of: mobile phones, PCs, speakers, hard drives, washing machines and more. Then map that to a global or even national total… it must be pretty substantial. But amid this heap of e-waste lies a goldmine.

Electronic products generally rely on a shared set of core materials, and a subset vital to their operation has received significant attention in recent years for their importance to the global economy. The scarcity of concentrated deposits, combined with the current concentration of processing facilities, acts as a chokepoint, seeing governments scramble to secure supply. That is critical minerals. As their name implies, critical minerals are a group of raw materials that are considered strategically important to a country’s economic or national security. They range from the likes of lithium, cobalt and nickel, essential for greater battery capabilities, to rare earth elements essential for a range of today’s technologies.[1] For instance, the rare earth neodymium is used to create high-performance permanent magnets, which are crucial for the miniaturisation of technology and in devices ranging from wind-turbine generators and missile guidance systems to satellite communications equipment. Critical minerals have few competitive substitutes for their desired applications, and are so essential for modern-day and frontier technologies that any supply shortages leave industries and countries vulnerable.

China currently dominates the refining stage of the primary supply (from mines) for most of these critical minerals, and has already shown that it will leverage its control over this chokepoint, imposing export controls on a number over 2025.[2] This drove up costs for sectors including defence, high-tech and clean-energy manufacturing, and sparked a flurry of activity from governments and companies seeking to diversity and secure their supply. One of the places that are now being urgently explored is the vast quantity of discarded electronic items, which are increasingly being recognised as potentially an accessible and large secondary supply.[3]

Unlike the key resource that has driven growth over the past 250 years, fossil fuels, the use of critical minerals does not necessarily deplete their global stock as they can be recycled[4] ‒ a fact which allows a circular economy, bringing a whole new dynamic to their supply situation. The ability to recycle and re-use the minerals, without substantial loss in quality, means that supply is less locked to deposits and geography. This has created a great opportunity for countries with high consumption of electronics and limited reserves of critical minerals to build their own domestic supply chains via their own e-waste, and in doing so reduce their reliance on foreign supply in the production of key technologies.

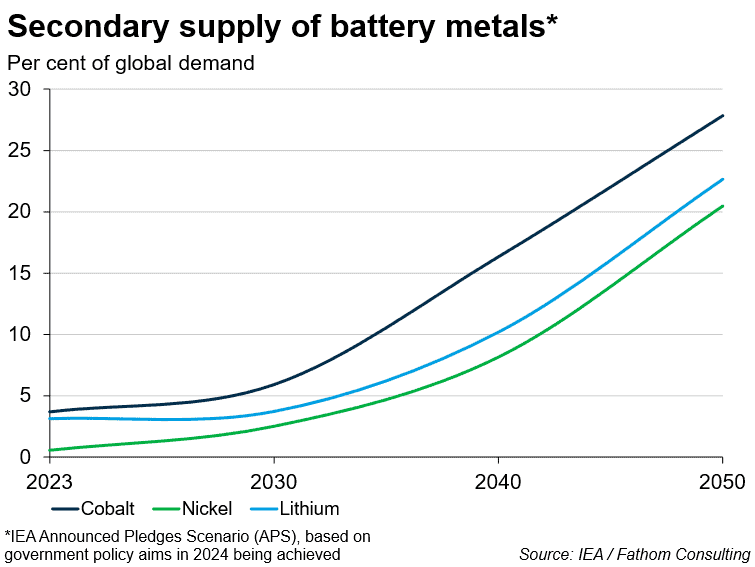

To quantify this, the International Energy Authority (IEA) has published a report on the recycling of critical minerals,[5] which estimates that the secondary supply of lithium, nickel and cobalt from recycling batteries could meet over 20% of global demand for each element by 2050, based on government policy aims in 2024 being achieved. For Europe specifically, the scenario sees secondary supply from battery recycling meeting 30% of its lithium and nickel demands by 2050. This is something not to be sniffed at, especially when you consider that demand for these materials is forecast to keep growing; it could also help to limit environmental damage from mining and processing.

The development of this secondary supply is already under way. The likes of Apple have developed proprietary robots[6] to allow recycling partners to safely disassemble various iPhone models to maximise material recovery. Meanwhile, recycling rates for critical minerals in electric vehicle (EV) production have grown rapidly in response to increased long-run demand.

The countries with the most to gain from this type of urban mining are developed countries that have high consumption of high-tech products, and so already possess significant ‘deposits’ of critical minerals. This abundance ought to provide a natural incentive to invest. To exploit this ‘natural’ opportunity to provide greater supply chain security, developed economies would need to store e-waste and establish local recycling operations, extraction and refining.

The starting point for these developed economies to diversify away from China is not strong, however. Although their collection rates for e-waste are high relative to the rest of the world (around 50% for Europe, US and Canada), they are weak in fundamentals for downstream processes. For one thing, they still represent the largest exporters of e-waste. More importantly, China also appears to be a key player in fundamentals of the secondary supply; it stands as a leader in necessary areas, such as recycling technologies and material recovery capacity.[7]

More by this author

Cognitive dissonance on the escalator

[1] The US has produced its own list of critical minerals here: https://www.usgs.gov/programs/mineral-resources-program/science/about-2025-list-critical-minerals

[2] This is not the first instance: China limited rare earth exports to Japan in 2010 following a fishing dispute, and in 2023 it started placing controls on antimony, gallium and germanium exports.

[3] One of the traditional problems with critical minerals such as rare earths is that although they are abundant within the Earth’s crust concentrated deposits, that make mining operations more viable, are limited.

[4] While fossil fuels are broadly considered as non-renewable the emitted carbon dioxide can be recycled for sustainable fuel, but at high cost.

[5] International Energy Authority’s (IEA) report on the recycling of critical minerals: https://www.iea.org/reports/recycling-of-critical-minerals

[6] Daisy to manage primary disassembly; Dave for handling of the Taptic Engine to recover tungsten and rare earth magnets; and Taz to separate magnets from audio modules.

[7] China has accounted for close to 74% of global patent filings in battery recycling technologies from 2014 to 2021. (https://policy.desa.un.org/sites/default/files/publications/2025-07/fti_2025_july.pdf and has been projected by the IEA to retain 80% of global pre-treatment capacity and 75% of material recovery capacity in 2030 for battery recycling.