A sideways look at economics

As we finalise our latest Global Economic and Markets Outlook, I have been thinking a lot about how other people make their own economic forecasts: it turns out we cannot make ours without taking a view on that. Read on to find out why!

The expectations of firms, households and investors are central to the macroeconomic models used by central banks, and by others in the business of making economic forecasts. The New-Keynesian Phillips Curve (NKPC) is a case in point. In its simplest form, the NKPC defines inflation as the sum of expected future inflation and a measure of output relative to potential. Under this textbook approach, and I would contend in the real world too, inflation depends in part on expectations about future inflation simply because neither wages nor prices can be adjusted continuously in real time. For example, when Fathom enters into a long-term contract with a client the price specified in that contract is usually fixed for at least a year, and often for longer. In those circumstances, it’s in our interest to take a view not just on any capacity constraints that we might face, but on how rapidly prices in general are likely to rise (or indeed fall).

How do people with little or no interest in economics form their expectations of future economic events? It’s a good question, and one to which economists, as a profession, do not have a firm answer. Up until the early 1980s expectations were often assumed to be adaptive: each period, one adapts one’s previous forecast by some portion, λ, of the previous period’s forecast error. This sounds sensible, right? At least there appears to be some learning going on here. However, there is a problem. If expectations were formed in this way, it would be possible to fool people systematically, period by period. Starting from a position where inflation was zero, and expected to be zero next period, a mischievous central banker might, for example, repeatedly raise inflation by a percentage point each period.[1] An individual using a process of adaptive expectations to forecast inflation would then underpredict inflation, period by period, by a percentage point, even if he or she set the learning parameter, λ, to 1.

Economists don’t like this idea. It makes them feel queasy. The so-called ‘rational expectations revolution’, associated with the work of US economist Robert Lucas, can be seen as a response to the problem outlined above. Under the rational expectations hypothesis, individuals use all the information available to them, which is often assumed to include a thorough understanding not only of how the economy works, but of how everyone else operating in the economy will behave, to come up with the best forecast that they possibly can. This may seem like a tall order to you. It does to me.

There is a third way. Rather than trying to come up with the best possible forecast, which would require considerable investment, people might just use a simple rule of thumb: an approach to forming expectations that, while not perfect, works well most of the time. If I was asked to forecast US inflation over the next year, and if I didn’t have access to Fathom’s suite of economic models, I might use the latest published data on inflation and work from there. Then I might think about the rate of inflation that policymakers are trying to deliver in the long run. Seeking to avoid controversy, because this is intended to be a light-hearted blog post, let’s assume that is the current inflation target. Next, whenever the latest published figure for inflation differed from the rate specified by the target, I might make take account of the level of concern expressed by policymakers at this discrepancy: do they seem in a hurry to get inflation back to target, or not? Finally, I would factor in, fairly informally, any other information I had to hand that might be relevant to the inflation outlook. Has the dollar just fallen precipitously, for example, or are there signs that aggregate demand is outpacing aggregate supply, creating shortages? What I would do, in short, is take a weighted average of the inflation target (2.0% at the time of writing) and the latest reading on inflation (5.4% at the time of writing), before making an ad hoc adjustment to incorporate the other information I had to hand. Algebraically, my rule of thumb for expected inflation in the next period would look something like:

Εtπt+1 = α + βπt-1+ Other stuff

α tells you my views about the rate of inflation that policymakers are heading for, while β tells you how urgently I believe they are trying to get there. What determines α and β? My α and β will change over time, influenced in part by the words and the deeds of policymakers.

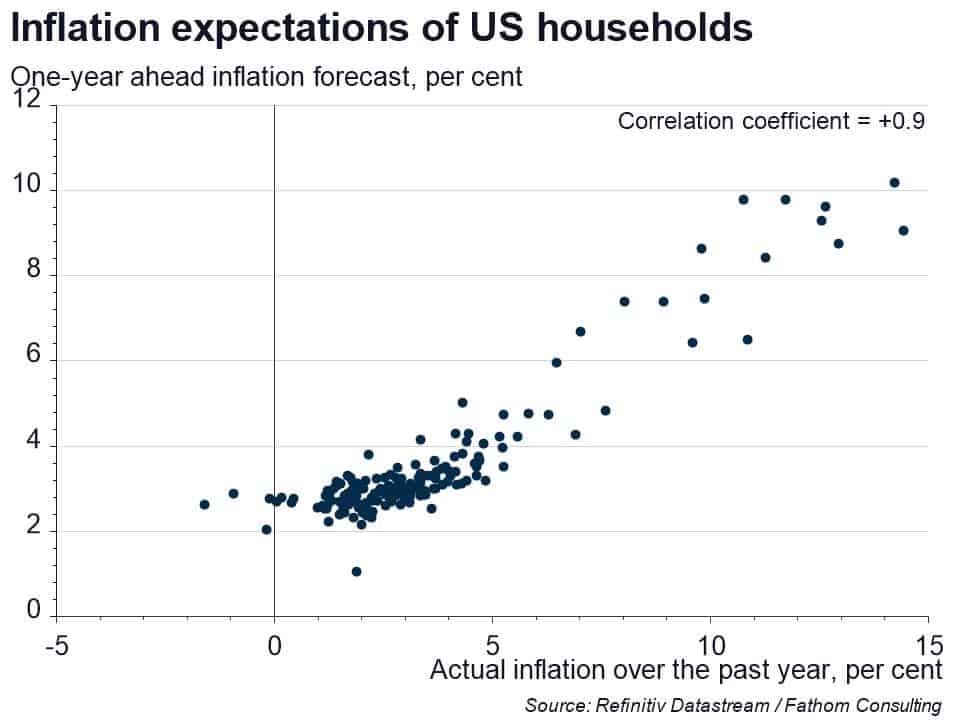

Empirically, we find some support for this ‘rule of thumb’ approach. Household expectations of US inflation, as surveyed by the University of Michigan, are heavily influenced by current inflation rates, as my chart shows.[2] The same is true of investors’ expectations measured by pricing in the US swaps market.

The fact that, in practice, many wages and prices are reviewed only infrequently means that expectations of higher inflation can become self-fulfilling: inflation is, itself, a function of expected inflation. We cannot be certain how firms, households, or investors form their expectations — of inflation or of other economic phenomena. My belief is that a good number of them will use the kind of rule of thumb I outlined above, weighing up the latest reading on inflation, and the rate of inflation that policymakers are aiming for in the long run, before throwing a number of other factors into the mix. There is a risk that the recent high rates of inflation seen in the US and elsewhere, which seem likely to persist in the near term at least, combined with the efforts of some policymakers to dampen down expectations that policy rates of interest will change any time soon, start to affect the way people form their expectations of future inflation. That is what would turn a temporary pickup in inflation into a sustained one. Of course, that may be no bad thing – but that’s a discussion for another TFiF.

[1] We assume, for simplicity, that central bankers are free simply to choose whatever rate of inflation they want, and then deliver it. They aren’t, of course, but many economic models ignore such real-world problems.

[2] Psychologists have argued that people tend to overweight recent events when thinking about what might happen in the future — so-called ‘recency bias’.