Headlines

- The euro area avoided contraction in the third quarter; with mounting headwinds, this looks to be delaying an inevitable recession

- Policymakers in some advanced economy central banks seem to be weighing the sluggish outlook for demand over still-high price pressures, raising the spectre of a DM central bank ‘pivot’

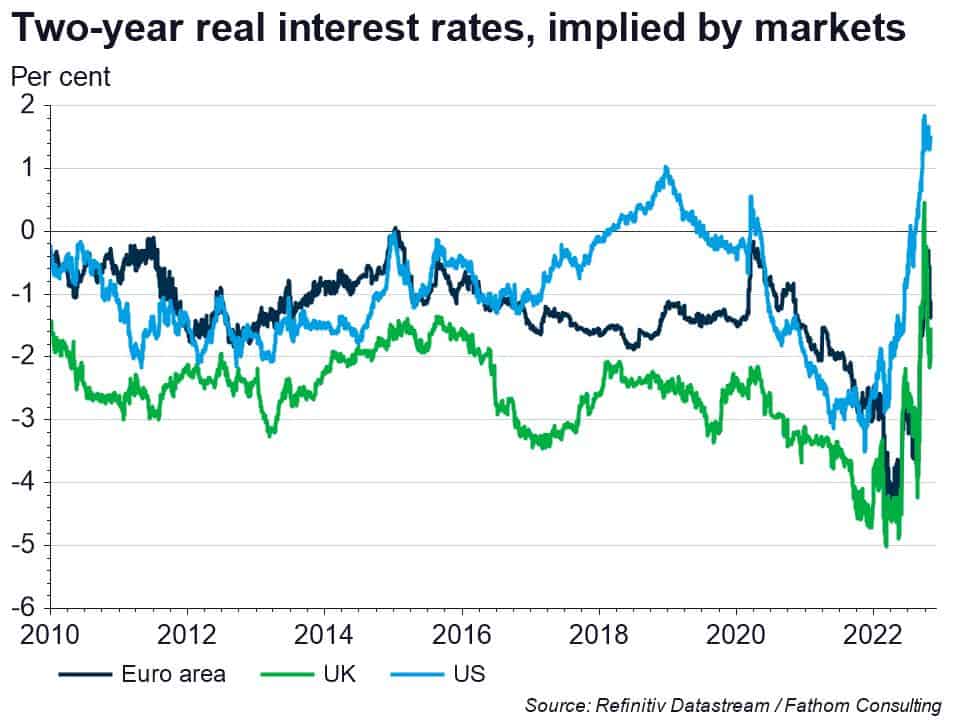

- Were that pivot to transpire, it would lead to a further decoupling with the US, where two-year real rates of interest are firmly in positive territory

- This combination of well above-target inflation and weak output offers a tricky landscape for investors: we will provide a more detailed assessment in our upcoming Global Outlook, Winter 2022

[Please click below to read the full note.]