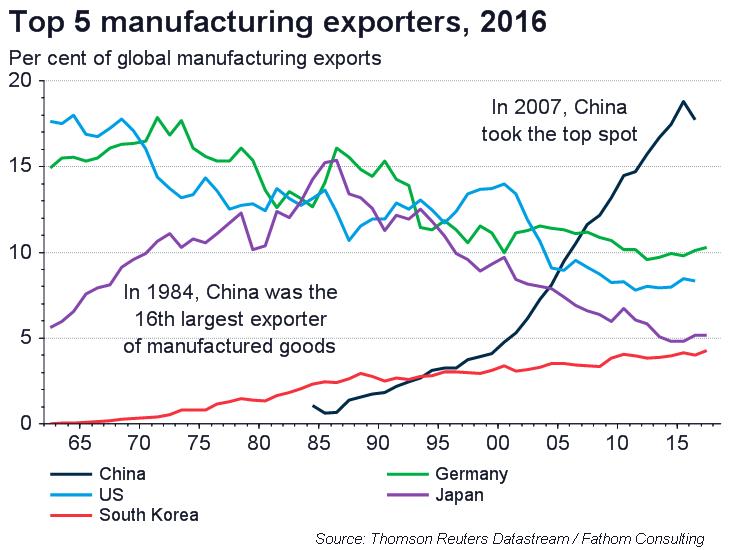

Our central forecast sees a global recession in or around 2020, driven by higher inflation, higher interest rates and sharp falls in equity prices. But there is another scenario, becoming increasingly likely, where inflation does not rise materially, for the same reason as it did not ahead of the financial crisis of 2008/2009: China. China then was distorting global growth by doing rapid industrialisation as a net exporter not – as it ‘should’ have been – a net importer. If it continues to distort in that way in future, inflation will not rise…