A sideways look at economics

A few sunny days in March are enough to do strange things to people. Coats come off, garden chairs reappear, convertible roofs go down, and someone, somewhere, confidently declares that winter is over. In Britain this is normally followed, within days, by a sharp reminder that it is not. The temperature drops, the heating goes back on, and everyone goes back to behaving as if they had never trusted the weather in the first place.

Markets have much the same habit.

They are always trying to identify the turning point: the last rate hike, the first cut, the start of a new cycle. This is understandable. Turning points are where narratives become neat and forecasts become marketable. It is much easier to tell a story about what comes next when one can first declare that what came before is finished.

The trouble is that economic seasons, much like the real ones, rarely end neatly.

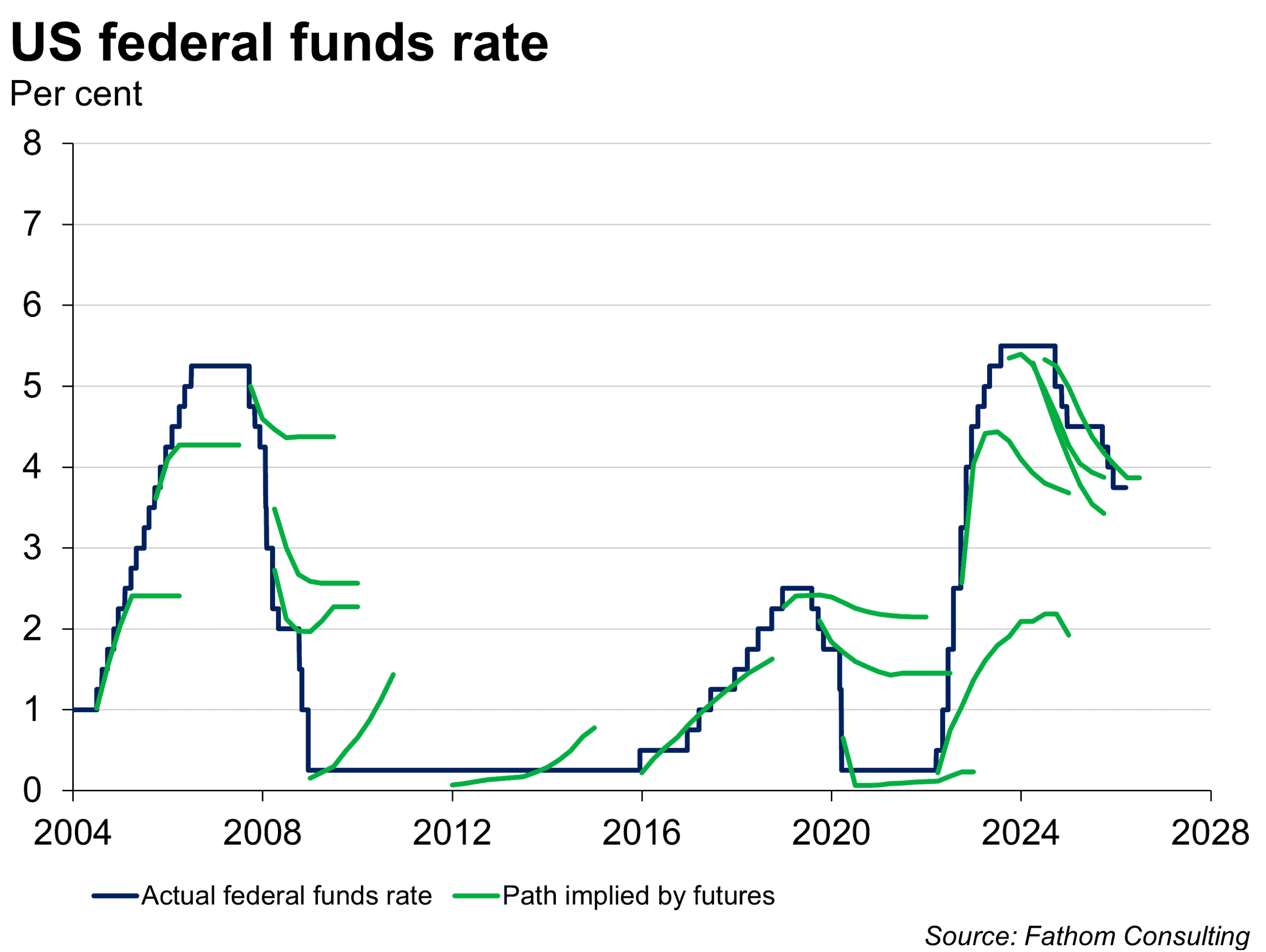

The chart shows this clearly. The blue line is the actual federal funds rate. The green lines show the path implied by futures at different points in time. Repeatedly, markets saw a turn approaching: policy tightening would soon stop, cuts would soon begin, a new phase was just around the corner. Repeatedly, those calls proved premature. With the exception of 2016 and the end of 2023 to the first half of 2024, most of these turning points turned out to be false starts.

That is not because markets are foolish. It is because they are human. We are naturally drawn to inflection points. We like the idea that things change direction in a clear and visible way – that there is a moment when winter becomes spring, when the bad run ends, when the hard part is finally behind us.

Part of the reason is that turning points make for better stories than slow adjustments. Saying that something has changed direction sounds decisive. Saying that it will probably continue in roughly the same way for a while, with a few interruptions, sounds vague and unsatisfying. Faced with uncertainty, people tend to choose the story that feels clearer, even if it turns out to be wrong.

Monetary policy is an ideal setting for this tendency. Interest rates sit at the centre of the economic narrative, so every new data release invites the same question: is this the moment when the cycle turns? If inflation falls, cuts must be coming. If growth softens, the central bank will surely react. If markets wobble, relief cannot be far away.

Under President Trump, investors have applied the same logic to his policies, assuming that if markets react badly enough, the next step will be softened – the so-called ‘TACO trade’. Each step looks like it could be the last one before the pivot. Very often, it is not. And that is exactly what the chart captures. Markets are usually right that the current phase will not last forever. What they tend to get wrong is the timing. The cycle runs a little longer than expected, the adjustment takes a little more time, and the turning point arrives later than the first confident forecast suggested.

The same pattern appears in everyday life. Winter does not end on the first sunny afternoon. Projects do not finish on the first deadline. Diets do not work after the first week. Even the feeling that life has finally become less busy usually lasts about three days before something else turns up. Change does come, but it rarely arrives as neatly as we expect.

That may be the real lesson. The mistake is not simply that markets forecast badly. It is that we all prefer a world with clear chapters: before, after, and the moment in between. In practice, most transitions happen in the uncomfortable middle, where nothing has quite finished but nothing feels the same either.

This does not mean the turning point never comes. The 2016 episode was one case where expectations were broadly right, and the expected policy paths at 2023-2024 turned out closer to reality than many earlier calls. But those successes stand out precisely because the broader pattern is different. We keep spotting spring in the first warm day, even though experience suggests winter rarely gives up without a fight.

By the time this blog is read, someone will almost certainly have declared that the cold weather is behind us. They may even be correct. But a little caution is usually wise, whether one is talking about the seasons or about interest rates. In both cases, the first sign of relief tends to arrive well before the change itself.

More by this author