A sideways look at economics

Do you know anyone who has suffered, or is suffering, from long COVID? I do, and it can be a very serious matter. In a broader, economic sense, though, we all are. Since COVID, economic sentiment across most of the developed world has been consistently in mild recessionary territory: the first time we have seen that pattern since we started collecting the data in the early noughties. This protracted ‘vibecession’ is not about growth, which is fairly strong in the US at least. Nor is it about financial markets which, until the war in Iran, were thriving, especially in the US. So what is it about? Jobs.

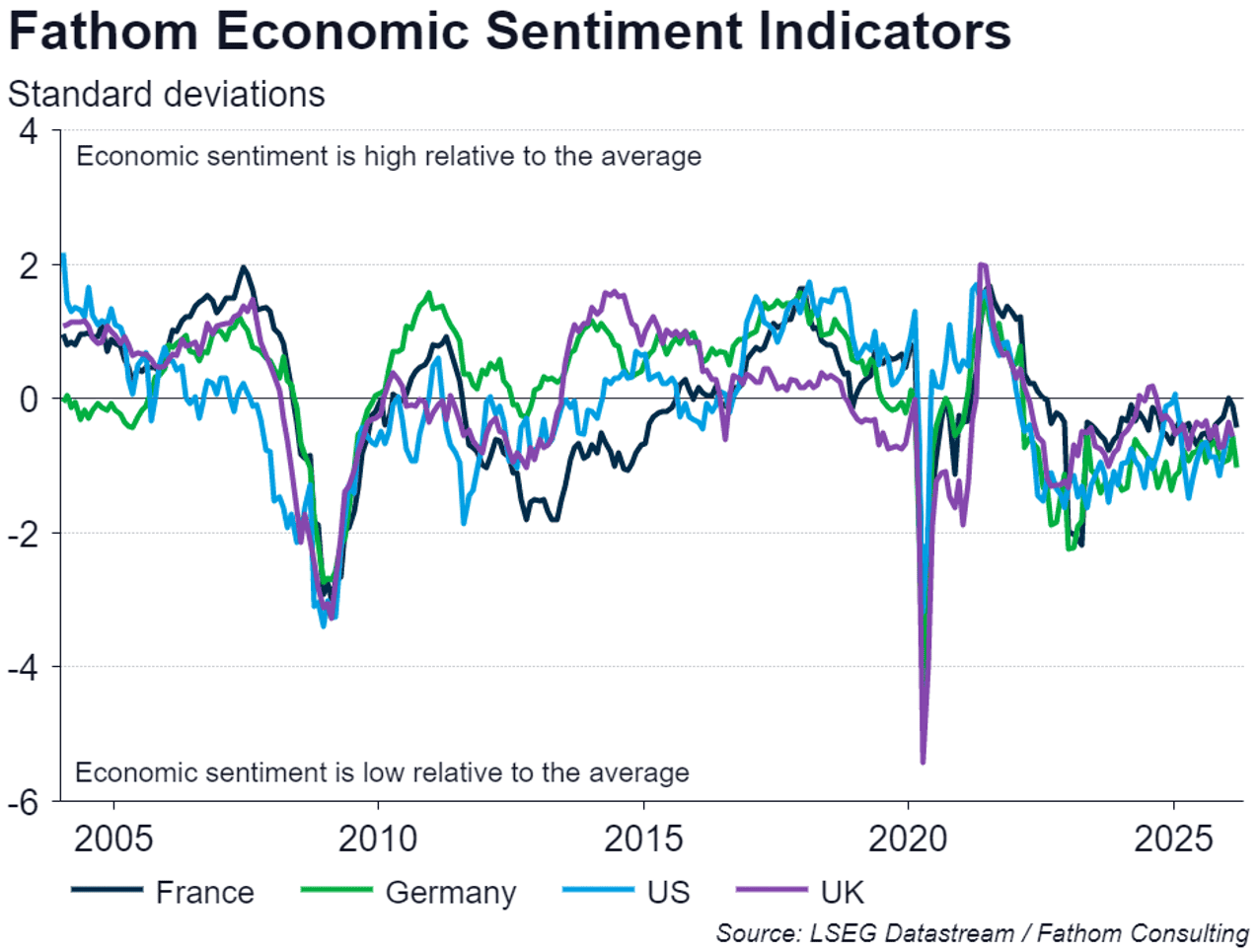

Even when it’s good, it’s bad. There is plenty of discussion out there about why. Some point to the so-called ‘K-shaped’ economy, in which asset prices and therefore those that own assets (disproportionately those with high incomes) do extremely well, while everybody else fares poorly. There is some truth in this account, although it suffers a bit from the assumption that the group of ‘everybody else’ makes up a big enough portion of the population to have a decisive impact on measures of sentiment; and yet does not benefit materially from higher asset prices. In the US, particularly, this is questionable, since direct equity ownership is much more widespread there than in other countries. Fathom’s measures of economic sentiment are pictured in the chart below, for the US, UK, France and Germany.

You can explore our global economic indicators in more detail on our data, models and tools page.

Focusing specifically on the US for the purposes of this TFIF, Paul Krugman argued, in a recent Substack post (Talking Vibes With Jared Bernstein – Paul Krugman), that the problem there is prices: not inflation, which has come down since COVID, but the price level, which has not. It’s certainly true that prices have not come down since COVID although, until the Iran conflict started, the rate at which they were increasing had slowed. But it is surprising, to me anyway, that people feel bad about high prices even though their income has generally gone up even further, so real incomes are generally substantially higher than they were pre-COVID. For higher prices to be the problem, then, would imply that people feel the price level more than they feel their own income. Seems unlikely to me.

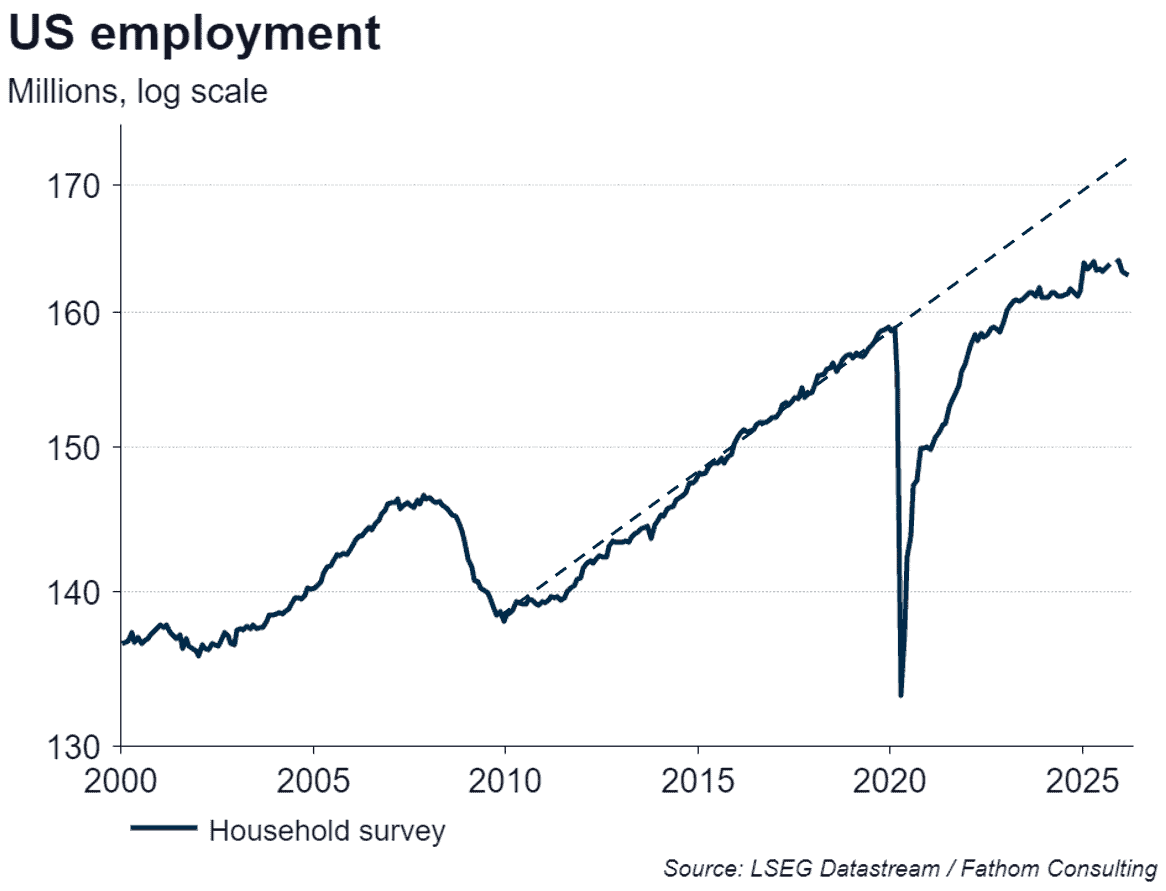

It’s not growth, and it’s not inflation or the price level (in my opinion). It’s jobs. What follows is a highly tendentious set of charts. I acknowledge this up front. It’s my best shot, for now, nonetheless. The chart below shows the level of US employment (according to the household survey), compared to a continuation of the pre-COVID trend in employment. (Why should that trend have been expected to continue? That’s the tendentious bit.) The gap is a shade over 10 million jobs, or about 6% of the participating labour force in the US. It feels as though there ought to be ten million more jobs than in fact there are.

If employment is so weak compared to the pre-COVID trend, why is unemployment so low? At 4.3%, the unemployment rate in the US is very close to our estimate of its equilibrium (the point at which it is exerting neither upwards nor downwards pressure on inflation). The answer is participation: COVID caused a significant proportion of the population of working age to drop out of the labour market altogether, and many of them have never come back.

Participation rates nosedived after the global financial crisis, but they were beginning to recover once real wage growth got under way from 2016 onwards. COVID brought that recovery to an abrupt end. It is plausible, though tendentious, to argue that the participation rate would have been two percentage points higher by now had it not been for (long) COVID. If there is such a shortfall, these are discouraged workers: people who would participate in the labour market if they judged it to be in their interests to do so. But this is still not enough: employment is still nearly 6% below where it would have been by now on its pre-COVID trend. Five and a half million discouraged US workers. What else?

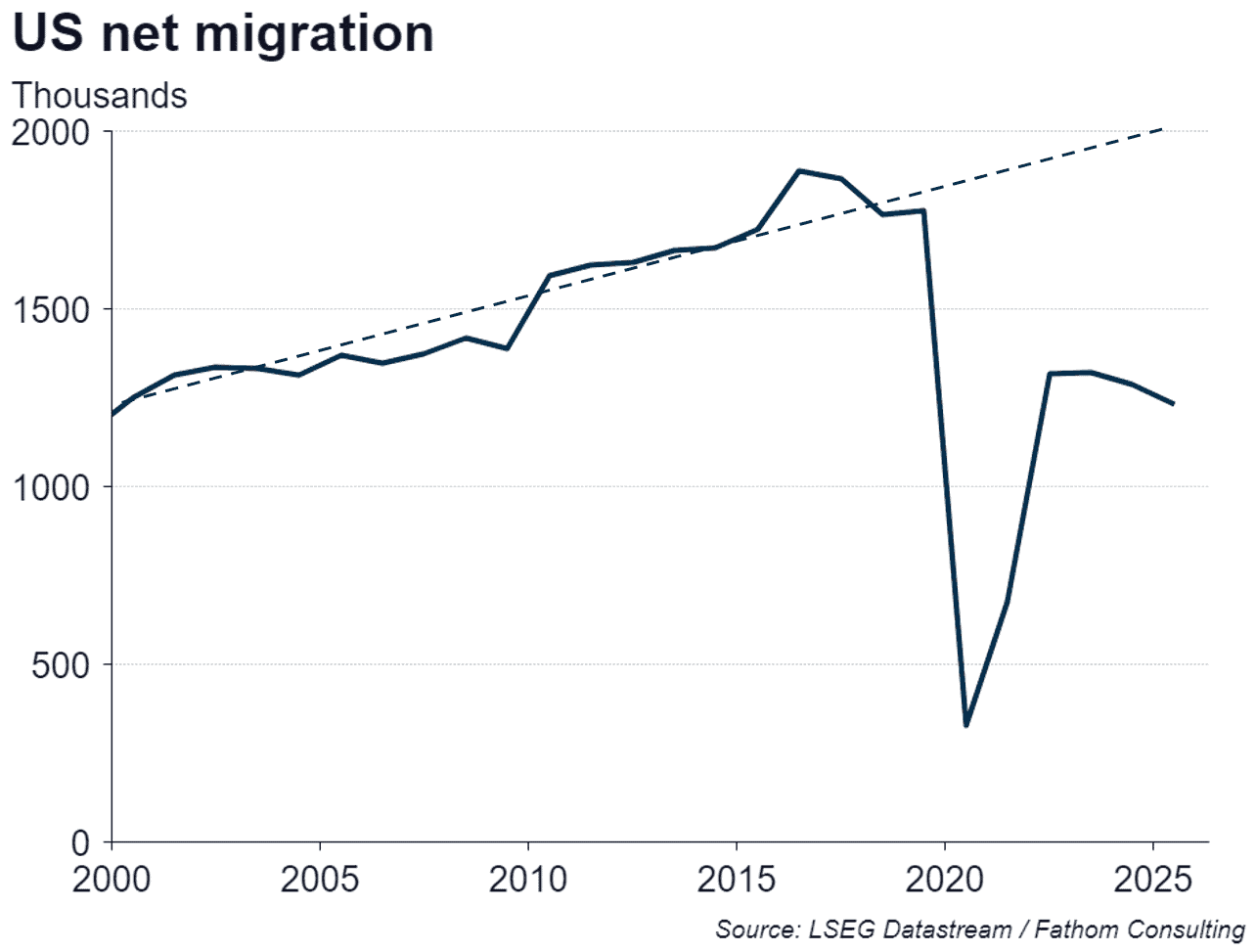

Most of the rest is down to migration. COVID caused net immigration to collapse, and the subsequent recovery, though sharp, never got back to where it previously was, never mind to where it might have plausibly reached had it followed the pre-COVID trend. The current administration is committed to keeping it relatively low henceforth. It is not clear how, if at all, a shortfall in net migration would affect sentiment for US citizens. But it’s possible that the shortfall contributes to an overall ‘chilling’ effect: the bar I normally go to is shut because they can’t find the staff; my cleaner has quit and I can’t find another…

Had net immigration stayed on its pre-COVID trend, there would be perhaps 5 million more people in the US, with a greater than usual proportion of those being of working age. Let’s say 4.5 million more people of working age. And the immigrant population of working age tends to have a higher-than-usual average participation rate: they emigrate to the US primarily to find work. Overall, therefore, this effect could easily have added an additional two percentage points to the numbers participating in the labour force. Their absence will be felt as a chill, perhaps; but also in the form of higher demand for non-immigrant labour. But, in spite of that, the participation rate has fallen as we have seen. The discouragement must be great.

So we have five and a half million discouraged US workers, and four million fewer immigrant workers. In addition, the increase in the unemployment rate since its post-COVID trough adds another 0.8% of the participating labour force, or 1.5 million people, unemployed. We’re over by about one million people in terms of the overall, ten-million shortfall in employment compared to the pre-covid trend, but that’s easily mopped up in measurement error for the nebulous concepts that we are discussing here (counterfactual expectations of employment levels and the like).

So, between a decline in participation rates, an increase in the unemployment rate and a reduction in inward migration, we get close to explaining the shortfall in employment in the US compared to its pre-COVID trend.

An unemployment rate of 4.3% feels OK: a rate of 8.3%, which is where it might have stood without the reduction in immigration (the short term effect of higher net immigration is to reduce the prevailing real wage by increasing the pool of unemployed participating labour: in the long term, that effect can disappear or even reverse) and the reduction in participation, would not. But that’s perhaps the truer picture; or at any rate the one that’s consistent with the vibes. 4% unemployment; feels like 8% with the post-COVID chill relative to expectations.

The question remains: why are potential workers so discouraged, given that real wages are increasing and already have increased relative to their pre-COVID levels? It could be that, during COVID, some of the unemployed got used to being unemployed, especially when there were cheques landing on their doorsteps at regular intervals. They became demotivated, as well as seeing their skills and training atrophy. These are so-called unemployment hysteresis effects, much discussed in the New-Keynesian literature. Or it could be that, while jobs are available, they are not the same jobs, or even in the same sectors, as the people made unemployed during COVID had previously occupied. I want a job: just not that job. Or it could be that the increase in the real wage that has occurred is specific to certain sectors or certain roles, which were not the roles occupied by those made unemployed.

These (and other) questions will be addressed in more depth in our forthcoming Global Outlook.

Further reading

Global Outlook, Spring 2026: preview