A sideways look at economics

A late family friend named Martin, whom I once asked what he thought of a mutual acquaintance said: “I don’t know; I haven’t formed an opinion yet.” How long had he known this person? Twenty years. Well, almost ten years after the UK voted to leave the EU, I find I still haven’t really formed a strong opinion about the impact that Brexit has had. It’s not that I haven’t thought about it. It’s that a couple of other things have happened, too: more than a couple. So this note is an audit: impacts of Brexit on trade, growth, investment; impacts on the political settlement in the UK; and what’s next. Bottom line: we should stop whining about it and start dealing with more important issues, of which there are many.

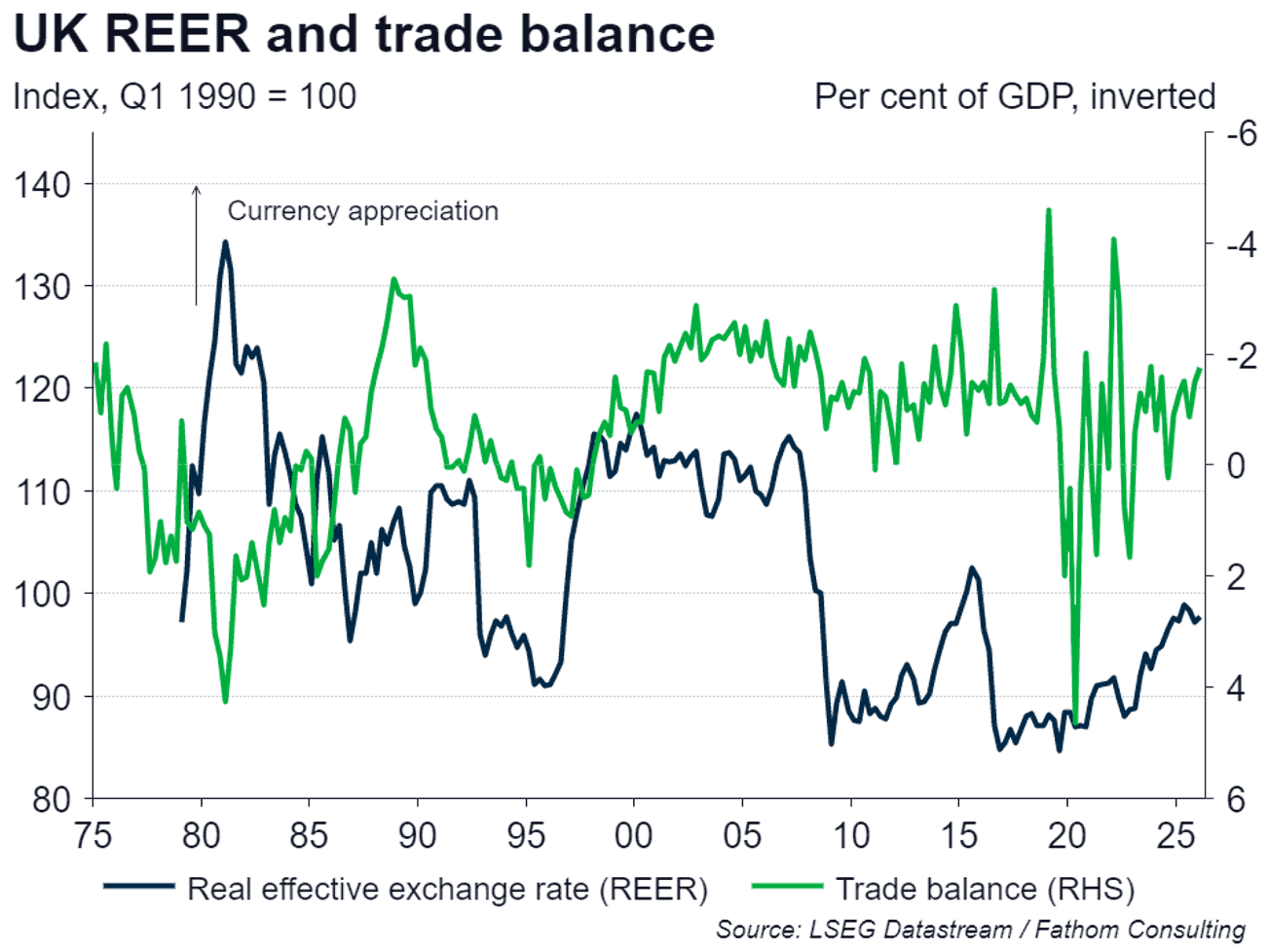

Let’s start with trade. The UK’s merchandise trade balance is in deep negative territory now, as it has been consistently since the late 1990s. The COVID period, followed by Russia’s brutal invasion of Ukraine created a huge amount of volatility in this number, and the Trump administration’s imposition of tariffs has muddied the waters even further. However, as the chart below shows, there is no clear evidence that the net trade position was made worse by Brexit, which officially occurred on the 31st January 2020, (nor is there evidence that it has improved).

Before we conclude that Brexit has not affected trade, though, consider the other line in the chart above, which is the sterling real exchange rate. The Brexit vote in 2016 saw sterling depreciate in real terms by 15% or so and it has still not recovered to its pre-referendum level, though it is close. A 15% devaluation should normally be associated with an improvement in the net trade position, but there has been no such improvement. Net trade should be less negative than it is: perhaps that shortfall is attributable in part to Brexit. Moreover, it’s not just a question of net trade: both exports and imports are probably lower than they would have been without Brexit, COVID, tariffs and the war in Iran. It’s the net trade position above that matters for aggregate demand. But it’s the gross position, arguably, that matters for the productivity of the whole economy, so it’s possible that Brexit has contributed, at the margin, to weaker productivity growth.

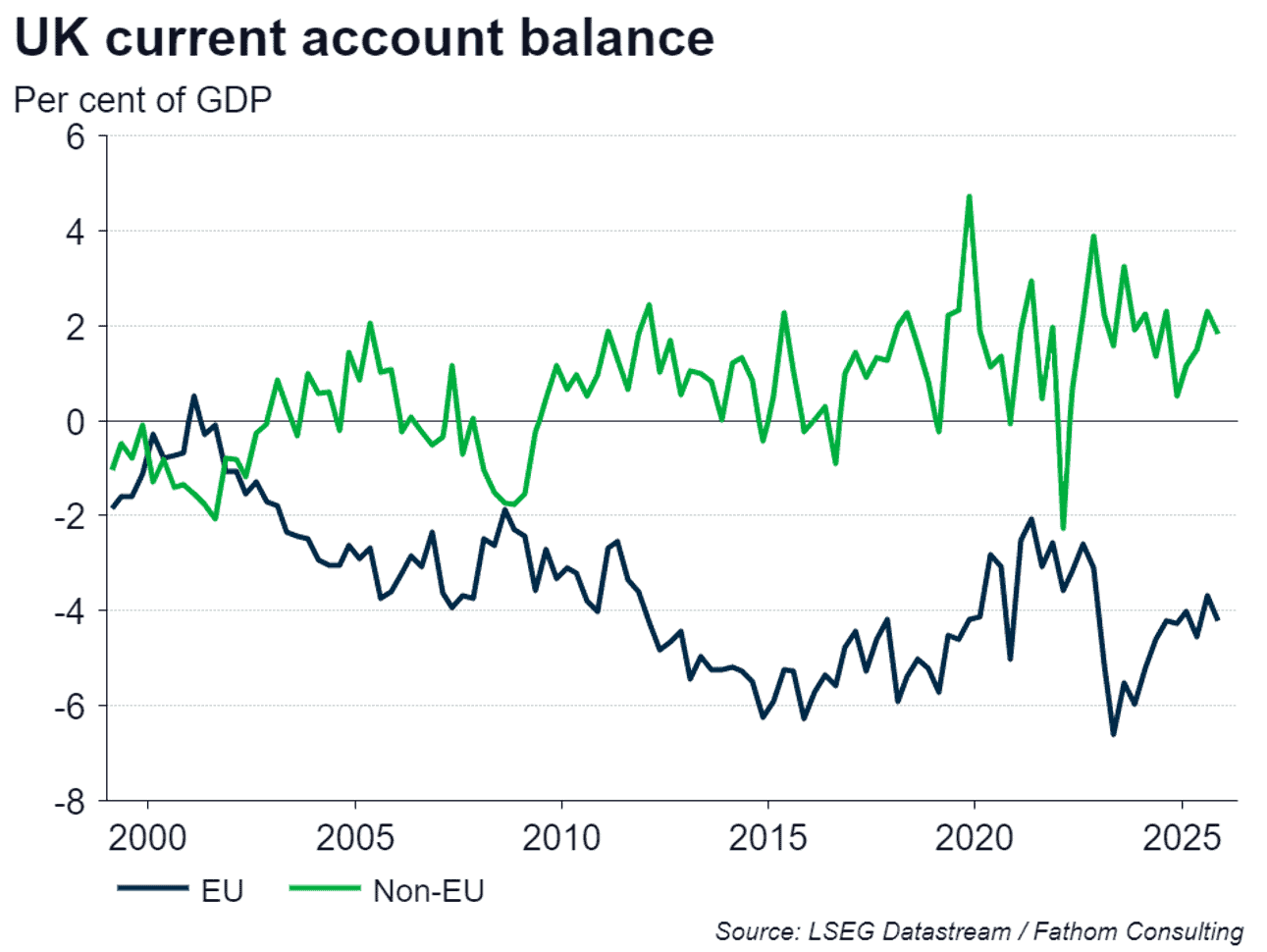

Merchandise trade is not everything, of course. But, even looking at the overall current account position (including trade in services as well as goods), the picture still shows no clear deterioration or improvement post Brexit. Notably, that’s true even for the UK’s current account position vis-à-vis the EU specifically, which is awful, but no worse that it was before Brexit. (If anything, it’s marginally less bad.)

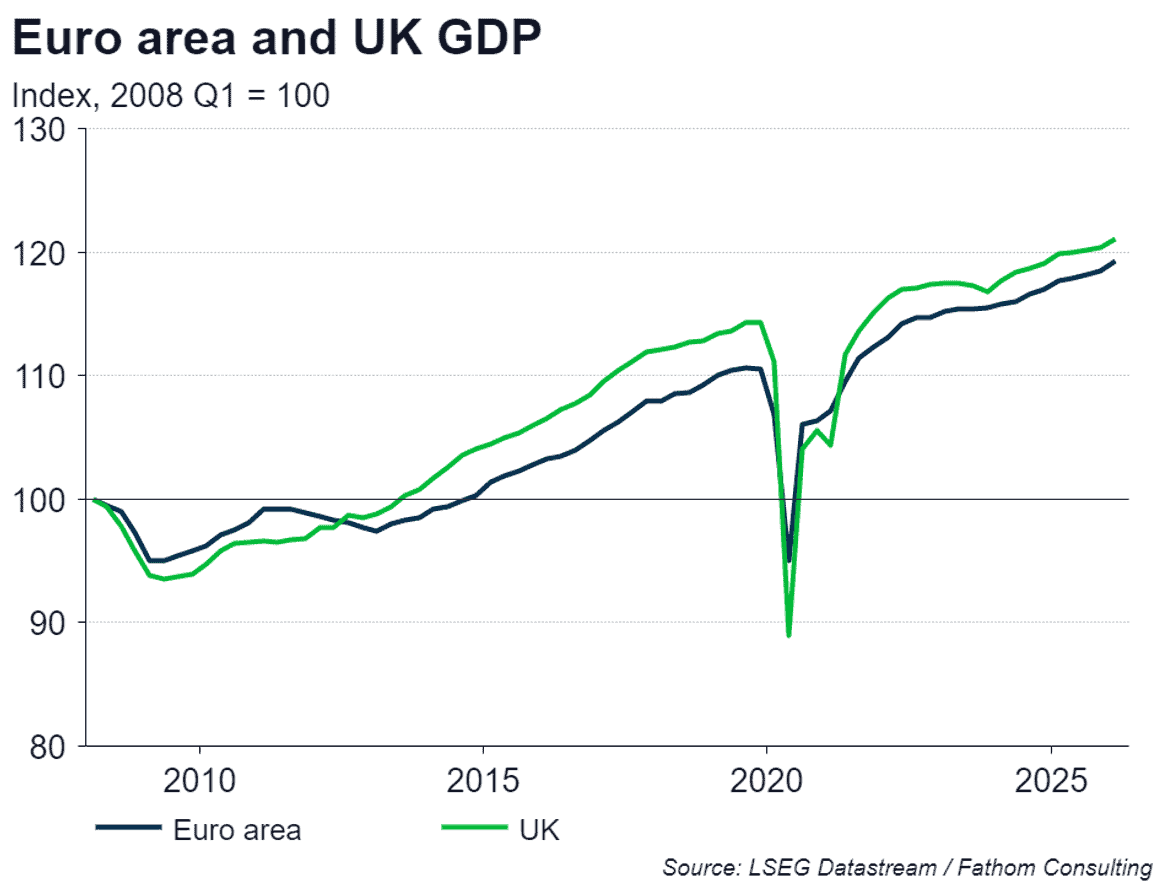

So, if the impact on trade and the current account position is unclear, what about GDP? Something similar holds. The UK’s GDP performance since 2008 has been dreadful, and has got worse since 2020, which was when the UK actually left the EU. One difficulty is that that was also the start of COVID. Another difficulty: whatever is the matter with UK GDP, something very similar appears to be the matter with euro area GDP too, as the chart below shows.

Attribution is difficult, to say the least.

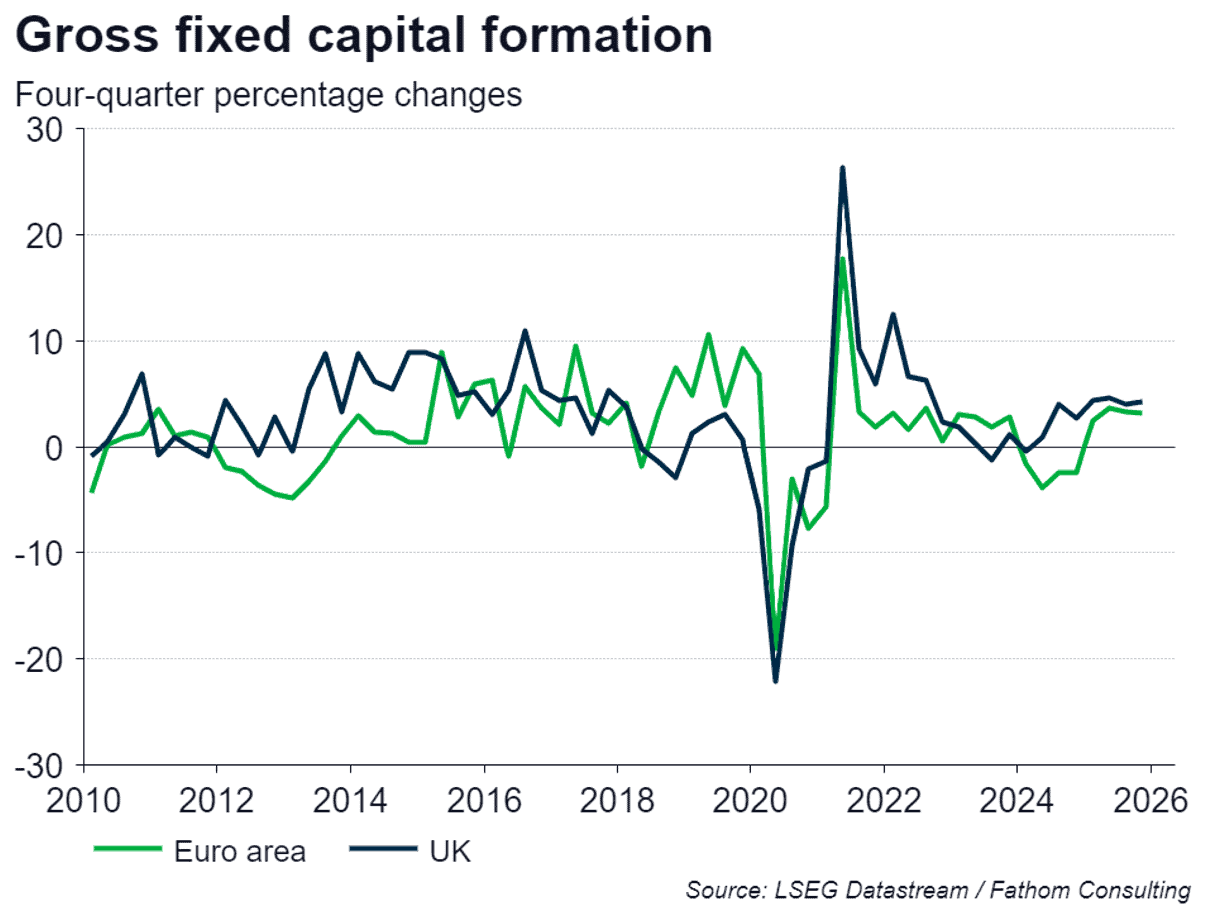

Both lines in the chart above show weak growth at best since the financial crisis, but there is very little to choose between them. The euro area had a sticky patch after the financial crisis as the euro crisis developed, but has basically tracked the UK ever since. If there is an impact of Brexit that differentiates between the UK and the euro area, it is not visible here. Neither is it visible in the comparable patterns for fixed investment, as the chart below shows. After the Brexit vote, there was a period when UK fixed investment growth was lower than that in the euro area. But, since COVID (and since Brexit actually happened), there have been two periods when the reverse was true. I defy you to point to the impact of Brexit.

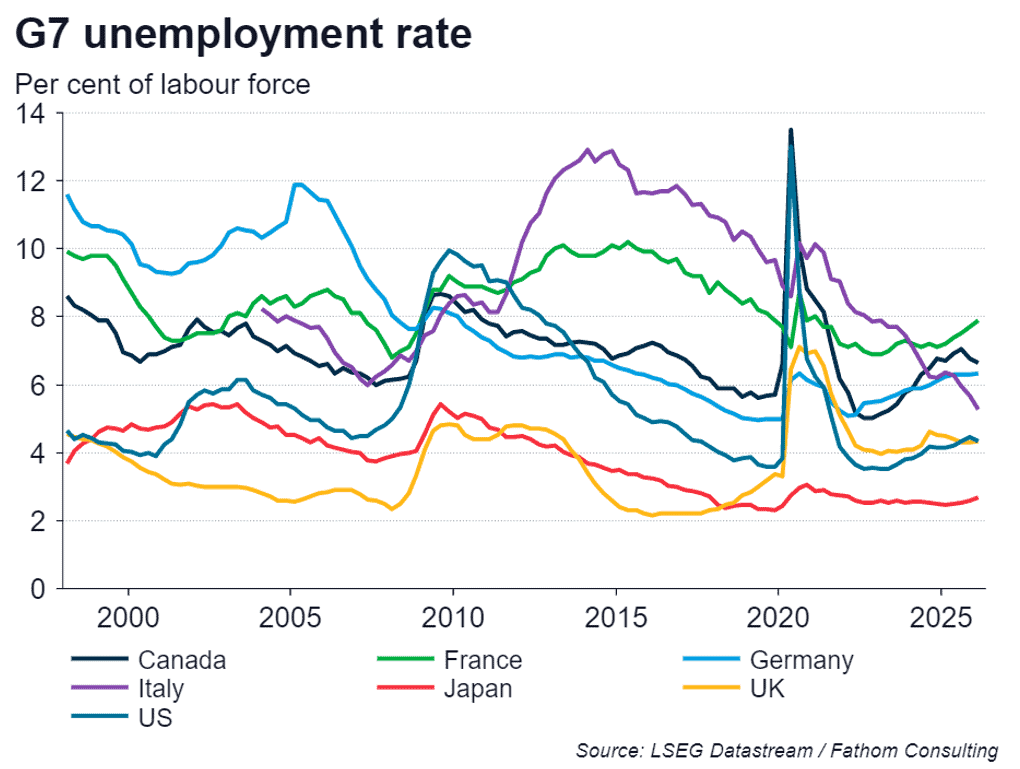

There just isn’t any clear evidence of a Brexit effect in trade, investment or growth. What about unemployment? Same again. The chart below shows the UK unemployment rate compared to other major economies. UK unemployment has increased, but it remains towards the bottom of the pack.

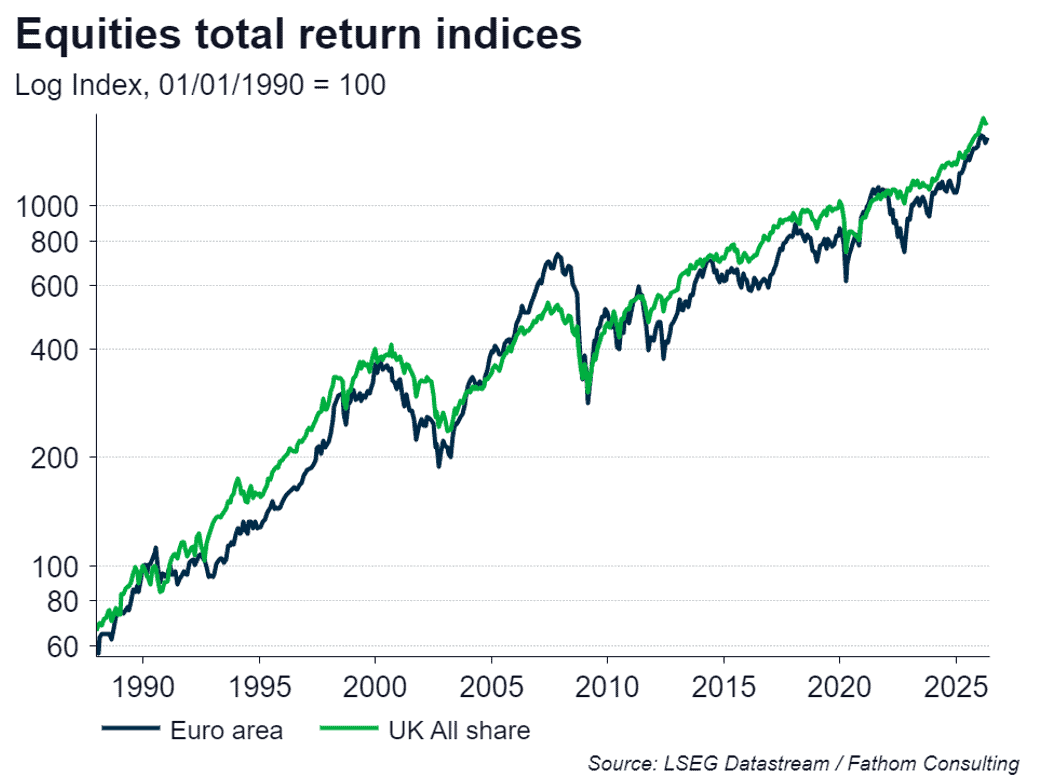

I just cannot see any impact of Brexit in the data, not clearly. And neither can financial markets. The chart below shows the total return on UK and euro area equities since 1990. The UK has outperformed slightly, but there is no visible impact of Brexit on either measure.

My TFIF (Just not feeling it? The vibecession explained: it’s the jobs stupid) of two weeks ago showed that there is no noticeable difference between the gloom felt by UK consumers and firms and that felt in other major economies. So, was Brexit all a lot of fuss about nothing? Not quite. When I cast my vote in the referendum, I was moved primarily by the impact that leaving would have on my freedom of movement in future, and that of my children. On that, I can report (as can many others, though not all) that movement to European destinations has become substantially harder since Brexit. And the option to move there for long periods of time, or even to choose to live there, has been made far more difficult. That option had value for me, whether I exercised it or not.

Net immigration to the UK has increased sharply since Brexit, though the principal geographic source of that immigration has changed from Europe to the rest of the world. Speaking for myself, I don’t have strong feelings either about the rate of immigration overall or its composition in terms of where the immigrants come from.

On the other hand, the political polarisation on the issue of Brexit, which increased sharply on many measures around the time of the referendum and for the few years after that until Brexit was actually achieved is now, if anything, reducing, at least according to this fascinating article by Houde and Stockwell. Other studies (such as this one) suggest that, while so-called culture wars remain hot, the strength of party affiliations is waning, and that the single issue of Brexit, for a while, took their place, becoming bound up with people’s sense of identity in the way that being a Labour or a Tory voter used to but no longer does. Overall, I take a small amount of comfort from this: Brexit was and is a divisive issue, but the energy in that issue is dwindling gradually; and the traditional sources of division have diminished substantially (the frequency of changes in the occupant of Number 10 in recent years, and the dismal performance of both the traditional ‘major’ parties in recent elections are testimony to this).

At the time of the referendum, I wrote a TFIF (52 shades of Brexit) that anticipated some of these changes: the introduction of a new dimension into British politics has changed the political calculus from vying for the median voter in a single dimension to a much more complex, fragmented landscape. That is where we now live.

I try, like our family friend Martin, to be guided by the facts when making judgements about people, or events. I don’t always succeed: some issues are so tightly bound to my sense of who I am that I can’t really step away from them and look at them objectively. And the other difficulty is that, as Martin found, ‘the facts’ rarely speak with one voice and have the annoying habit of changing over time.

One thing I hope I’ve learned is that the sense of outrage that I sometimes feel, on learning that someone else has taken a different view than myself, is rarely justified by a cool assessment of the facts. This note has shown (to my satisfaction anyway) that most of the antagonism around Brexit, the most divisive issue of our times, was misplaced. I hope that the gradual diminution in polarisation on this issue can continue, and we can get on with dealing with pressing problems such as boosting our military capability and finding a route back to productivity growth. Both of these are feasible, but first we need to stop fighting the battles of a decade ago.

The detailed prospects for the UK economy will be addressed in more depth in the UK section of our forthcoming Global Outlook. If you are interested in hearing more on this subject, please enquire here for a free presentation.

Further reading

A new dimension in British politics

UK Update: when the facts change

Idea that Britain cannot afford to arm itself is dangerous nonsense

The charts and data featured in this blog are available to LSEG clients through Chartbook on Workspace, and to Fathom clients directly through our Client Zone. To learn more about accessing Fathom’s data, models and tools, get in touch with us here.