A sideways look at economics

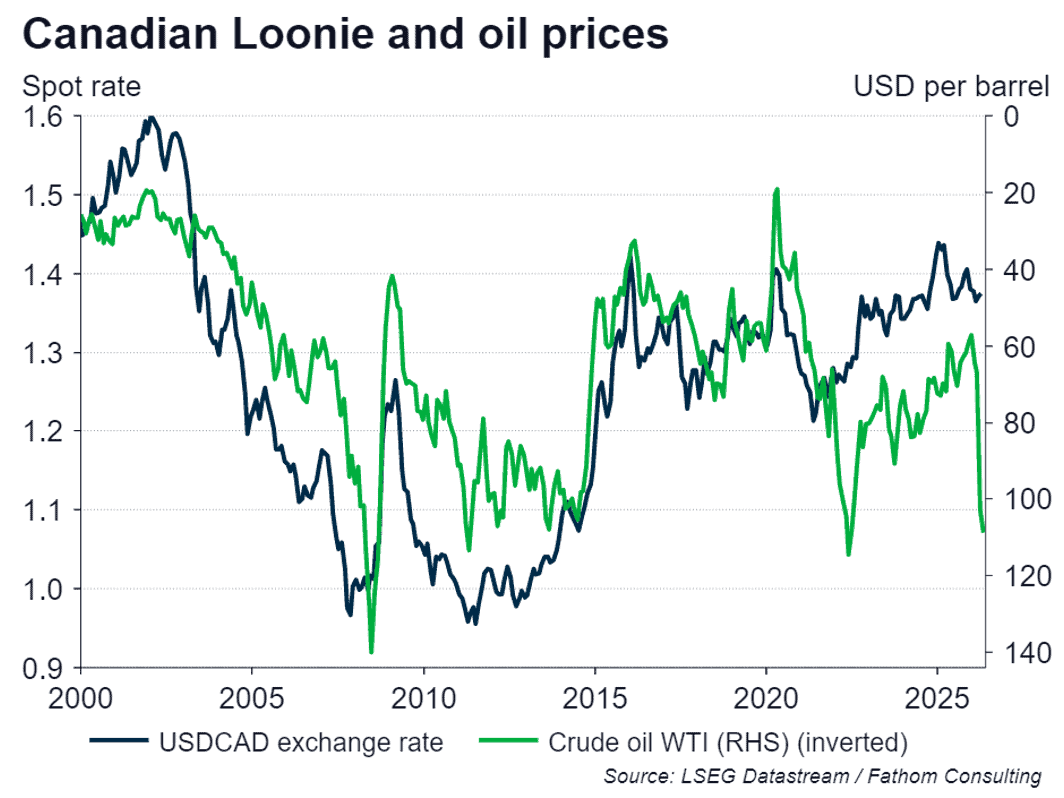

Until President Trump took office for the second time, one of the most-reliable relationships in foreign-exchange markets was between the value of the Canadian dollar and the price of oil. When oil prices rose, so did the Loonie, making Canadians richer as a result. Since oil is priced in US dollars, a stronger Loonie meant Canadians did not get so much Canadian currency in exchange for their oil as they otherwise would have; but they got more of everything else. This is how so-called petro-currencies work. However, since the start of the war in Iran, either FX investors are leaving a lot of money on the table, or something fundamental has changed. What might that be?

The Loonie moves with the price of oil. Kids learn this at primary school[1]. The chart demonstrates the fact: but what’s going on right now? The Loonie should be trading around 1.20 to the US dollar, but it’s closer to 1.40. It’s unlike FX investors to be so forgetful.

It could be that FX investors do not believe that the current price of oil is going to hold. That would track with oil futures (in ‘backwardation’, implying futures prices are below spot prices, which can be interpreted as markets expecting the spot price to fall) and with how equity traders seem to be pricing the Iran war: soon over, quickly forgotten. While this benign outcome cannot be ruled out, in our view it is only a 15% shot. A continued lack of clarity, with flip-flopping in the expressed intentions of the US and Iranian administrations, and frequently changing intensity of the conflict, seems the much more likely scenario to us: and a sharp deterioration, which would see oil spike to $170pb or beyond, is also more likely than a swift resolution. So I’m not really buying this line.

Perhaps investors feel that if the price of oil stays high, or rises from here, the global slowdown that it will induce would offset any additional revenues that Canada might accrue in the short term. If oil stays high, it means there has been a negative supply shock to the global economy: a restriction on the physical quantity of oil that can be consumed. The impact of such a shock is different than if it were a demand shock: China’s increasing appetite for oil after its accession to the WTO in 2001 was unambiguously good news for oil exporters like Canada and for the Loonie. Supply shocks are more difficult to read. However, it’s a supply shock happening to oil supplies from another region, not one that is distributed evenly across all suppliers including Canada. If anything, that structure should be particularly helpful to Canada’s terms of trade. So I don’t subscribe to this view either.

Perhaps the dominant factor in the minds of FX investors is the rise in global risk induced by the war in Iran, and the safe-haven properties of the dollar in that context, rather than the impact of the war on the price of oil. There might be some mileage in this account. I can see how the impact on the Loonie might be smaller in this environment that it might otherwise have been. But I remain surprised that the impact is effectively zero.

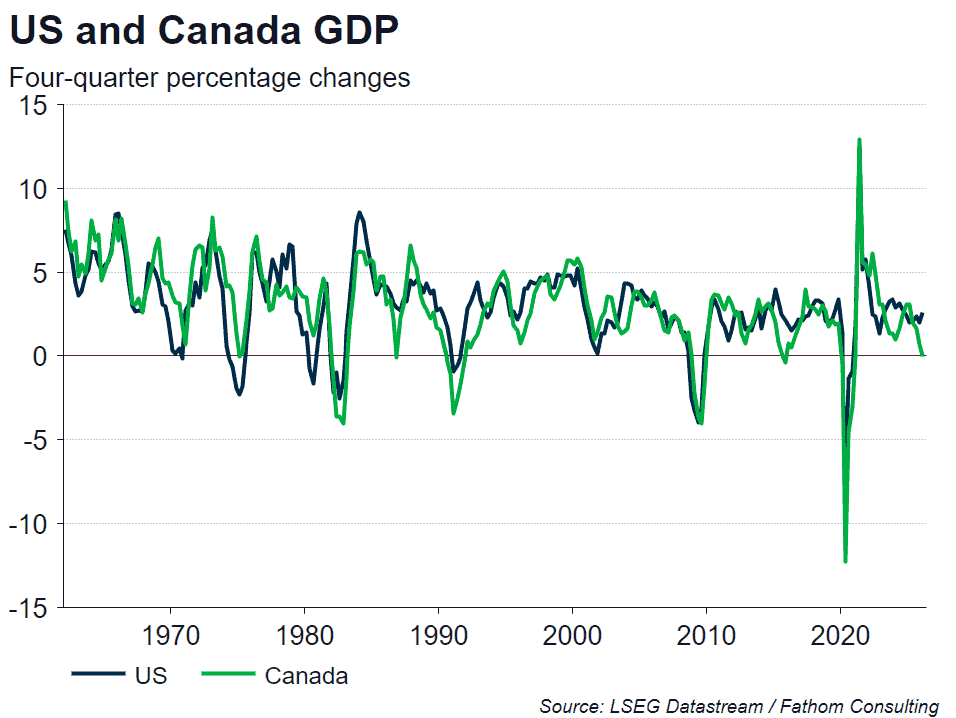

Or it could be that something dramatic has changed investors’ perceptions of Canada. If so, it’s hard to see what it is in the data. The chart below shows how Canada’s growth tends to track that of the USA. If anything, that relationship is even tighter and better defined than the relationship between the Loonie and oil prices. There is no sign here that anything has changed, for all the sound and fury about Canada from the Trump administration. The two countries remain in lockstep.

Another candidate explanation is that US tariffs are somehow dampening the impact of oil prices on the Loonie. The Trump administration did select Canada for special attention when tariffs were first introduced. But, since then, tariffs have fallen to only 10%, much like the rest of the world. There has been no noticeable impact on Canada’s production or exports of oil. So it’s a stretch to assert that this is why the Loonie / oil price relationship has stopped working.

I think it’s something else, though I should warn you that this is a low-conviction call, for now. I think it’s a sense of unfinished business between the US and Canada. Trump was extremely vocal on taking office about how Canada should become the 51st state of the USA. That would be the natural thing, according to him, for a country that has no realistic alternative to the US security umbrella. Since then, the gaze of his administration has switched, to Greenland, to Europe, to Russia, to China, to his domestic agenda and, most recently, to Iran. Speaking for myself, though, I cannot shake the feeling that it will flit back to Canada in due course.

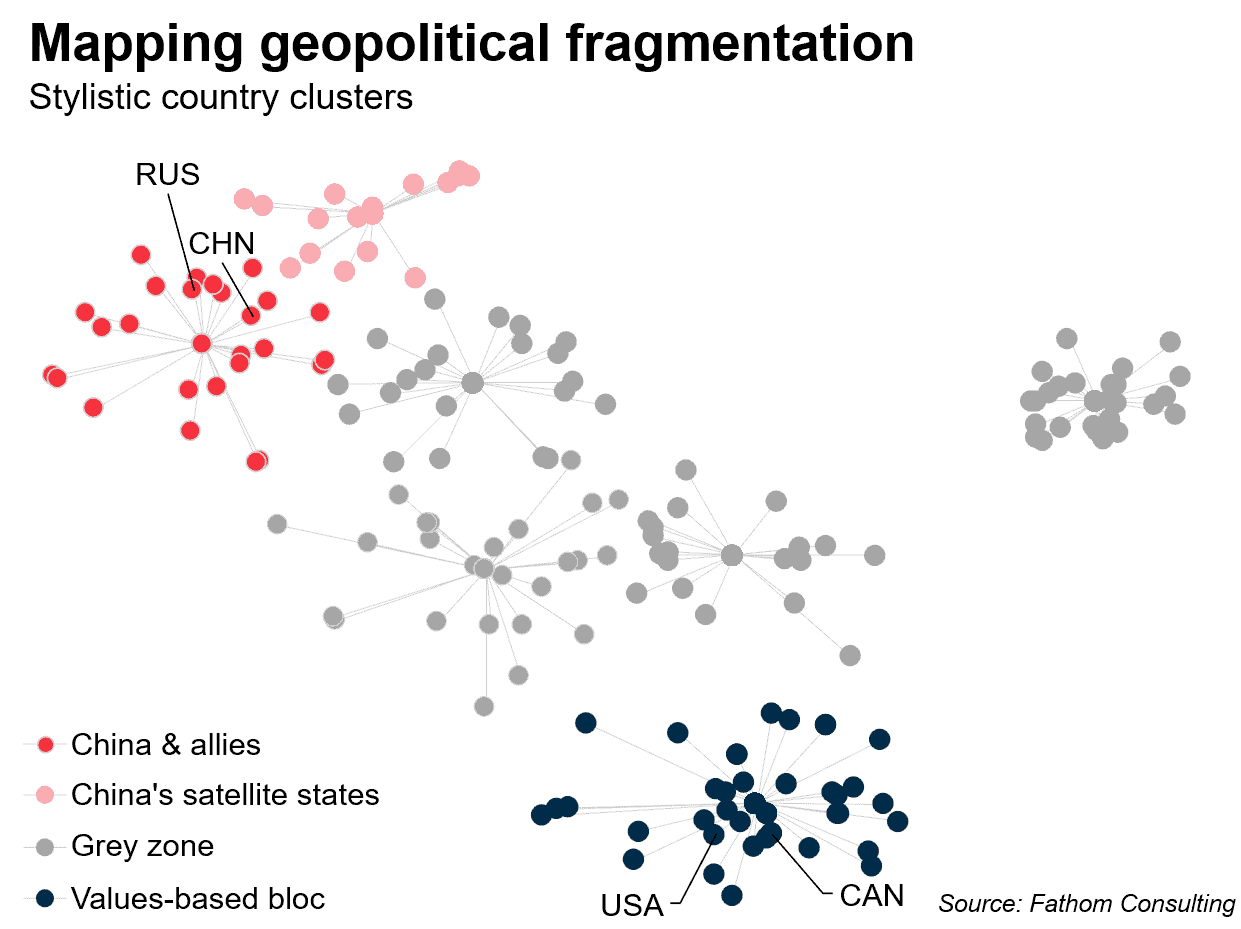

Trump has called time on the post-war geopolitical settlement. If he follows through on that thought, it will have profound implications for everyone, but perhaps most of all for Canada. The graphic below shows how countries cluster together, based on a proprietary measure of likeness that reflects the choices each country has made in response to 24 geopolitical flashpoints over the most recent decade or so.

There is a clear red corner and blue corner in this picture. Using data up to 2024, Canada and the USA were extremely closely aligned in the blue corner, along with most of the major European economies and other advanced economies. If Trump follows through on his rhetoric, that picture is about to change. It could be that the USA peels off from the blue group into an area of its own: in that case, will Canada follow it? If so, it will be the 51st state de facto, if not de jure. Or will Canada stay put, alongside Mark Carney’s proposed group of ‘middle powers’? And, if it makes that choice, on whom will Canada rely for its defence? Can it safely rely (in Mark Carney’s words when he was Governor of the Bank of England) on the kindness of strangers, for something so fundamental as defence?

In Europe, the major economies (particularly Germany) are dramatically increasing their defence spending, and that reality is reflected in the equally dramatic outperformance of European defence stocks: this move is real, it is happening now, and it is very likely to continue into the long term. Canada has increased its defence spending sharply since Mark Carney took office. But, for now, Canadian defence stocks do not appear to be reacting. Bombardier is up, but no higher than the peak it reached in 2018 (and far lower than preceding peaks). And other Canadian defence stocks (CAE, for example) are performing adequately but no better than that. I think this is because investors are not buying the pivot towards increased defence spending as sustainable in the long term, because it is not clear what it achieves: not yet (although it probably also reflects the fact that Canada has few if any ‘pure’ defence stocks, and such as it has are small by comparison with US or European competitors, so they might not benefit dramatically from increased defence spending). Canada could contribute meaningfully to increased military capability as one among a group of middle powers; but no such group currently exists. On its own, even if it were to double its defence spending, it could effectively deter small aggressors, but not big ones. It can do that already.

As things stand, it is just not clear what the future holds for Canada. The other middle powers are, at least publicly, silent on Carney’s Davos challenge to them. The USA has yet to act on its rhetoric. In that context, I’m not surprised that the Loonie is static, even in the face of much higher oil prices. The other shoe has yet to drop, and the Loonie is not moving until it does.

The next week or so will probably prove me wrong. But that is my take, for now.

Will Carney get his way and prompt the emergence of a meaningful group of middle powers? That’s a question Fathom has addressed in the context of a Table-Top Exercise (TTX), one of an increasingly diverse and interesting range of TTXs that are now an important delivery mechanism for our research: find out more about our service here. The exercise called on Fathom’s proprietary measures of geopolitical alignment, which identifies countries’ geopolitical alignment and ways to influence it. These and other themes are developed in our Global Outlook: if you’d like a free trial, please apply here.

Further reading

Global Outlook, Summer 2026: preview

Hormuz block: an oil price shock scenario

Idea that Britain cannot afford to arm itself is dangerous nonsense

The charts and data featured in this blog are mostly available to LSEG clients through Chartbook on Workspace, and to Fathom clients directly through our Client Zone. To learn more about accessing Fathom’s data, models and tools, get in touch with us here.

[1] Don’t they? Pretty sure they do. Right after fractions, basic FX market fundamentals. They should anyway.