A sideways look at economics

The Japanese term ‘Kaizen’ has been co-opted by Western management consultants and lifestyle gurus, and is taken to mean a culture of continual improvement: tiny, incremental changes, day after day that, after a long period, mean success. I vividly remember being shown around a Japanese-owned factory in the UK, where the management had recently presented one of their employees with a reward for having found a way to shave 1.7 seconds off the time it took him to complete one of the processes he controlled. That 1.7 seconds, aggregated up for the year, and spread across all their factories globally, would return a cost saving in six figures annually. It’s a Japanese term, but it has almost never applied to the Japanese economy as a whole. The Japanese miracle saw enormous growth post-war, nothing incremental about that. The bubble economy saw ballooning asset prices. The subsequent correction saw growth stagnate, demographics deteriorate and debt soar. Now, another change is afoot, possibly a huge change. Kaizen may apply in some parts of the Japanese corporate sector but not to the macroeconomy, which is characterised by something more like Kaikaku – sudden, radical change.

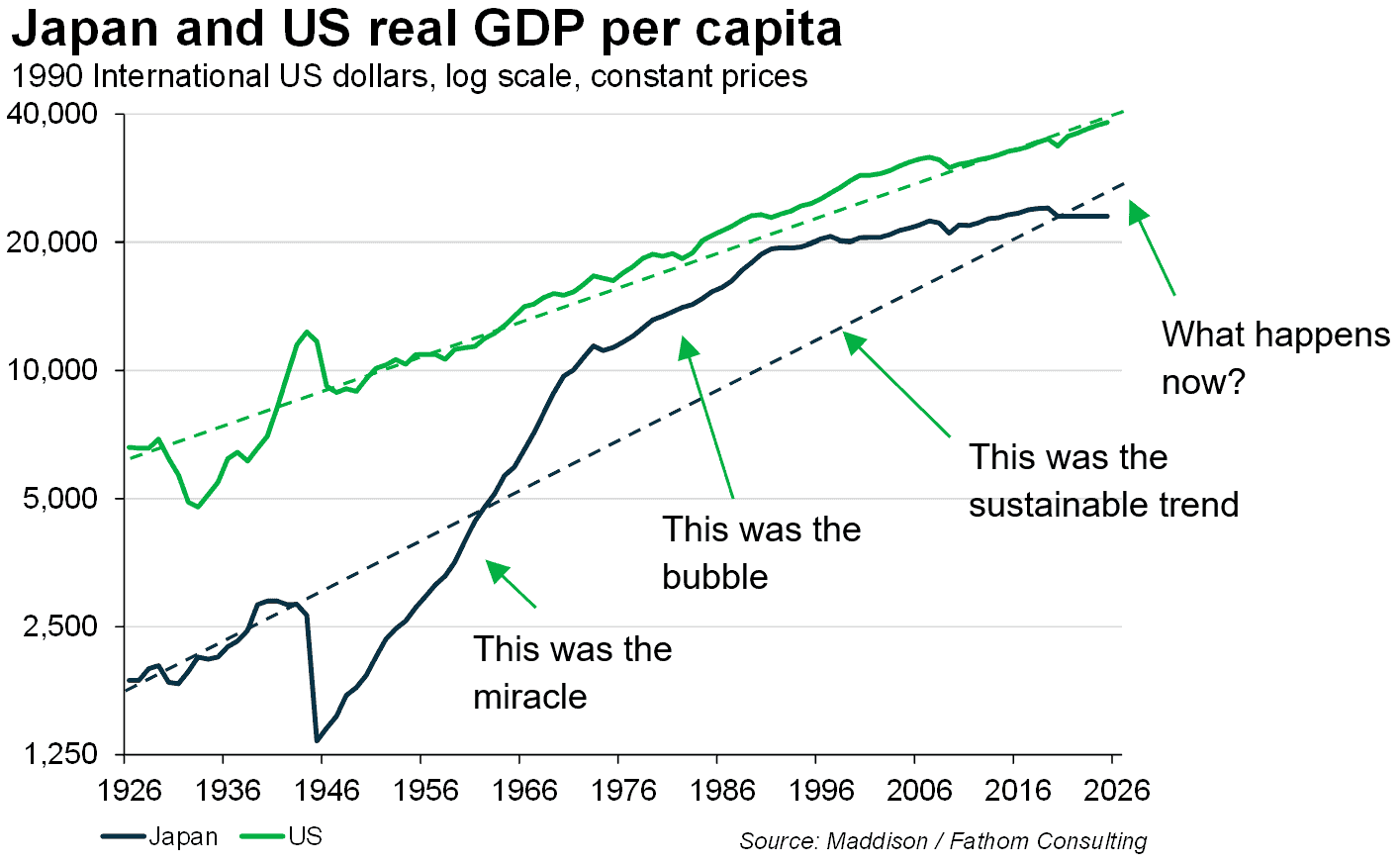

The Japanese economy has seen a series of huge changes over the last several decades. The post-war miracle. The bubble economy. The bursting of that bubble. The lost decades thereafter. And, just recently, the level of Japanese per capita GDP has finally converged on what might reasonably be described as its very long-run trend, as the chart below illustrates. Does this herald another huge change? Rapid evolution in debt dynamics suggest: maybe.

After the bursting of the bubble economy in the late 1980s, the Japanese government embarked on a kind of Ponzi scheme. In a true Ponzi scheme, there is no underlying asset at all, just an ever-increasing pyramid of new entrants to the scheme paying the existing members. But government debt markets can have Ponzi-like characteristics too (and not just in Japan, by the way), in which ever-increasing debt is issued against an underlying asset that is not growing, or might even be shrinking in value. The asset in this case is the Japanese economy and, specifically, the tax base that represents for the Japanese government. In cases like this, the same logic ultimately applies as in a pure Ponzi: eventually, new entrants to the scheme will not arrive in sufficient numbers and the scheme will collapse.

The collapse of a pure Ponzi scheme results in the members of the scheme losing the money they ‘invested’ and the principals going to jail. Here, the comparison with government debt markets breaks down: many other options are available. Over-indebted governments can choose: tighten fiscal policy and keep it tight (meaning decades of weak growth or no growth); find a new source of growth (sounds fun but, if we knew how to do that, we would have done it already); deliver repeated bouts of surprise inflation (which ought to be a contradiction in terms, except if people have very short memories), so the ratio of debt to nominal GDP improves even though the debt has not been paid down; engage in financial repression, so that investors are forced to accept sub-par yields on the debt that they acquire; or default.[1]

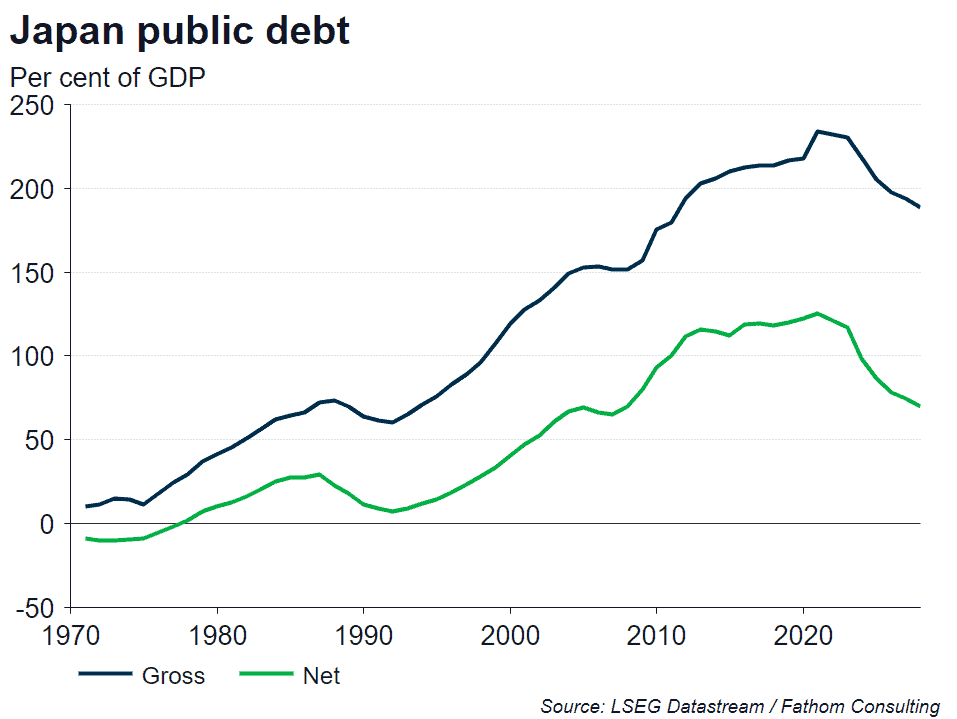

In Japan, it is starting to look as though they have chosen a mixture of inflation, financial repression and default, of a sort. Their hand has been forced. The equilibrium that allowed the Ponzi scheme to keep growing has come to an end because, in a sense, the supply of new entrants to the scheme has slowed. Unlike in the Bernie Madoff[2] scheme, where the new entrants included ill-advised Hollywood stars among others, the new entrants in the case of Japanese government debt are bond investors, whether Japanese or otherwise. The game changed during COVID, when it became apparent that inflation in Japan, dormant for decades, was not dead but merely sleeping. The COVID shock caused it to stir. The fact that it is still alive changes everything. Now, as a bond investor, I can see a way in which the Japanese government can effectively fail to pay me back: by accommodating further inflation. The government debt-to-GDP ratios in Japan peaked ahead of COVID and have fallen back significantly since then.

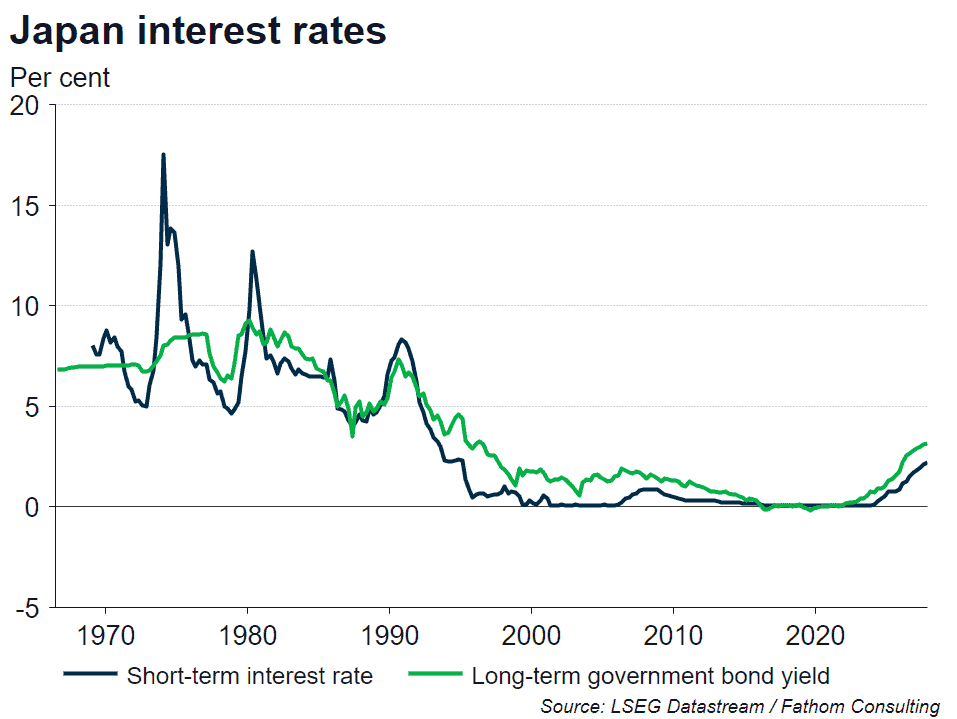

The COVID inflation has been extremely helpful to the Japanese government. But it has not gone unnoticed by bond markets. Now, for the first time really since the bubble economy, yields on Japanese government debt have increased materially, and that process has just begun.

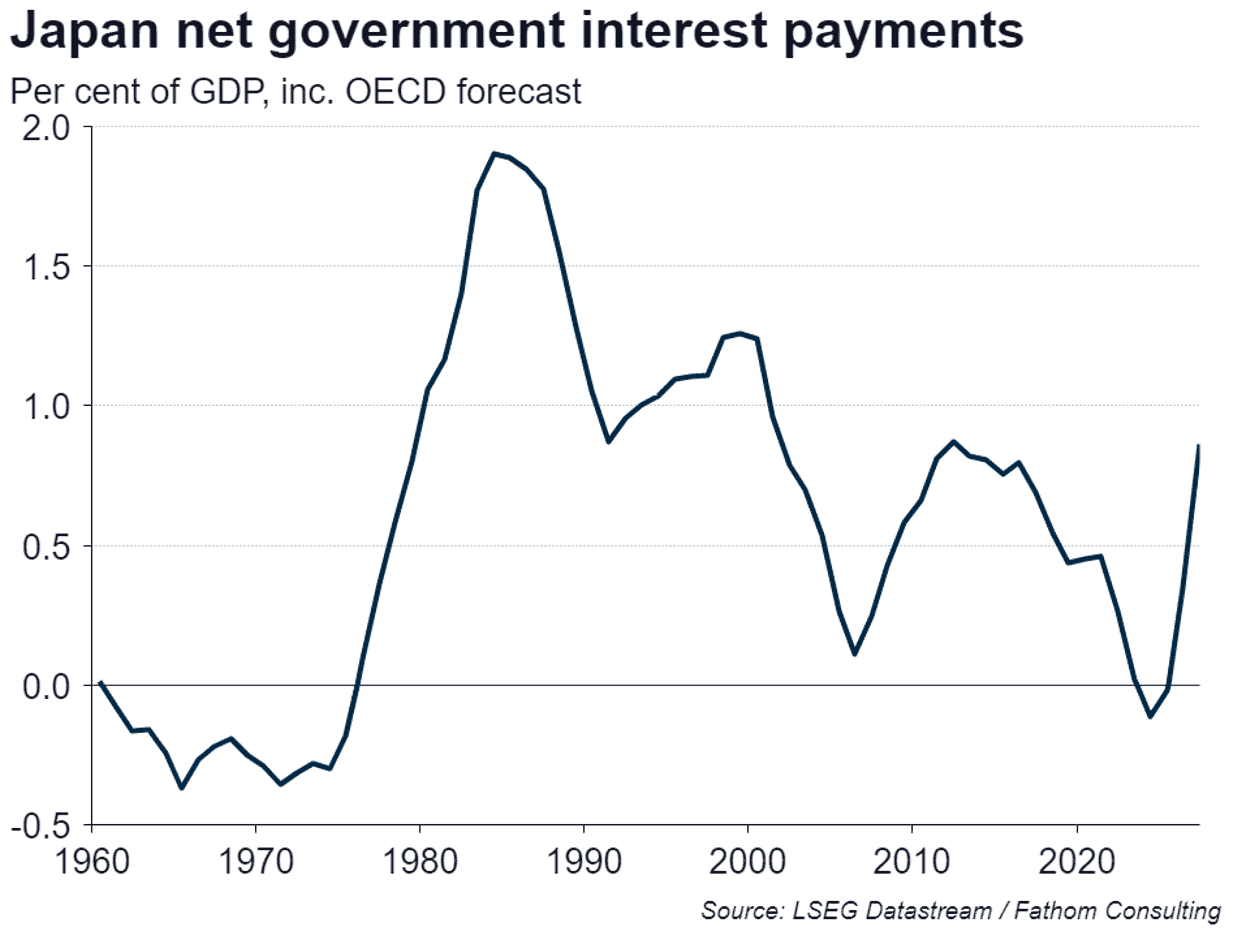

Higher yields mean higher debt-servicing costs, in the end. Japanese government net interest payments are rising for the first time in a long time as a result of higher yields, not as a result of increased borrowing. They are now as high as at any time since the Global Financial Crisis, and it is likely they will surge further in the months to come, to levels not seen since the bubble economy.

The government tried, for a while, to hold back the tide by implementing a strategy called ‘Yield-Curve Control’ (YCC, a fancy name for Quantitative Easing, which is a fancy name for the central bank buying government debt). But, as any builder of sand-castles knows, and as King Knut told us, the tide cannot be controlled. In the case of Japan, the effect of holding down yields on government bonds (once the inflation genie had been released by COVID) was to cause the yen to tank, losing over 50% of its value against the dollar within two years. A collapsing currency creates further impetus for inflation, helpful for debt ratios, but concerning (to say the least) for holders of nominal bonds. To arrest the decline of the currency, Japan abandoned YCC. The currency stabilised, but bond yields popped and they are still rising. The trend is accelerating. If it were to continue, the government will be forced into default. But that is a last resort.

The Japanese government will hope, no doubt, that with the currency stable, inflation will fall back, nominal bond yields will stabilise on their own, and the genuine hard work over recent years to bring the government’s primary fiscal balance (before interest payments) to zero will start to pay off. That is a possible outcome. But there are other pressing exigencies to consider: Japan has an urgent need to drastically increase its military capability (it can join the rest of the world in that). If it does so, watch the primary deficit balloon. If it doesn’t… well, that doesn’t bear thinking about.

The way bond prices are moving at the moment suggests a more dramatic scenario than a tame return to monetary stability is increasing in likelihood. Bond markets might choose to force the issue. If they do, then look for a return to YCC and a collapsing yen (unlikely to please the US); or for haircuts on holdings of JGBs. Kaizen, it ain’t. Kaikaku. Look it up.

These and other themes are developed in our Global Outlook: if you’d like a free trial, please apply here.

Further reading

Could financial repression help cut mounting debt?

Japan election landslide may deepen tensions with Beijing

Global Outlook, Winter 2025: a fiscal wreckoning for Japan?

Fathom’s charts and underlying data are mostly available to Fathom clients directly through our Client Zone and to LSEG clients through Chartbook on Workspace. To learn more about accessing Fathom’s data, models and tools, get in touch with us here.

[1] There are other options floated by some, such as ‘writing off the debt’, which normally means exchanging private holdings of debt instruments for cash. The difficulty with this is that cash is also a form of government debt: this mechanism (QE, for example) doesn’t deal with the problem, it just gives it another name. The government can still default (for example by declaring all cash to be worth half what it was worth the day before). And it can still inflate (achieving the same result over a longer period).

[2] https://en.wikipedia.org/wiki/Bernie_Madoff